IndiaFilings

Expert

Published on: Jul 30, 2026

Fcra Registration For Trusts And Ngos

Charitable Trusts, Societies,

Section 8 Company that receive foreign contribution or donation from foreign sources are required to obtain registration under Section 6(1) of Foreign Contribution Regulation Act, 2010. Such a registration under the Foreign Contribution Regulation Act, 2010 is called a FCRA registration. In this article, we look at the procedure for obtaining FCRA registration in India.Eligibility for obtaining FCRA Registration

Organizations seeking foreign contributions for definite cultural, social, economic, educational or religious programmes may obtain FCRA registration or receive foreign contribution through "prior permission" route. It is preferable for an FCRA applicant to be a Trust or Society or a Section 8 Company. The not-for-profit entity must have also been in existence for a minimum of three years while making the FCRA application and should not have received any foreign contribution prior to that without the Government's approval. Additionally, the entity seeking registration should have spent at least Rs.10,00,000/- over the last three years on its aims and objects, excluding administrative expenditure. Statements of Income & Expenditure, duly audited by Chartered Accountant, for last three years are to be submitted to substantiate that it meets the financial parameter.

In case a newly registered entity would like to receive foreign contributions, then approval for a specific activity, specific purpose and from a specific source can be made to the Ministry of Home Affairs through the Prior Permission (PP) method.

Criteria for grant of FCRA Registration

Once, an FCRA application is made in the prescribed format, the following criteria are check before providing registration.

The 'person' or 'entity' making an application for registration or grant of prior permission-

- Is not fictitious or benami;

- Has not been prosecuted or convicted for indulging in activities aimed at conversion through inducement or force, either directly or indirectly, from one religious faith to another;

- Has not been prosecuted or convicted for creating communal tension or disharmony in any specified district or any other part of the country;

- Has not been found guilty of diversion or mis-utilisation of its funds;

- Is not engaged or likely to engage in propagation of sedition or advocate violent methods to achieve its ends;

- Is not likely to use the foreign contribution for personal gains or divert it for undesirable purposes;

- Has not contravened any of the provisions of this Act;

- Has not been prohibited from accepting foreign contribution;

- The person being an individual, such individual has neither been convicted under any law for the time being in force nor any prosecution for any offence is pending against him.

- The person being other than an individual, any of its directors or office bearers has neither been convicted under any law for the time being in force nor any prosecution for any offence is pending against him.

The acceptance of foreign contribution by the entity / person is not likely to affect prejudicially –

- The sovereignty and integrity of India;

- The security, strategic, scientific or economic interest of the State;

- The public interest;

- Freedom or fairness of election to any Legislature;

- Friendly relation with any foreign State;

- Harmony between religious, racial, social, linguistic, regional groups, castes or communities.

The acceptance of foreign contribution-

- Shall not lead to incitement of an offence;

- Shall not endanger the life or physical safety of any person.

Applying for FCRA Registration

Application for FCRA registration can be made using Form FC-3. Along with the application, the following documents must be submitted:

- Self-certified copy of registration certificate/Trust deed etc., of the association

- Self-certified copy of relevant pages of Memorandum of Association/ Article of Association showing aim and objects of the association.

- Activity Report indicating details of activities during the last three years;

- Copies of relevant audited statement of accounts for the past three years (Assets and Liabilities, Receipt and Payment, Income and Expenditure) clearly reflecting expenditure incurred on aims and objects of the association and on administrative expenditure;

Once FCRA registration is granted, it is valid for a period of five years. An application for renewal of FCRA registration can be made 6 months prior to the date of expiry, to keep the registration valid.

Online FCRA Registration process

The procedure for online FCRA registration is explained here.

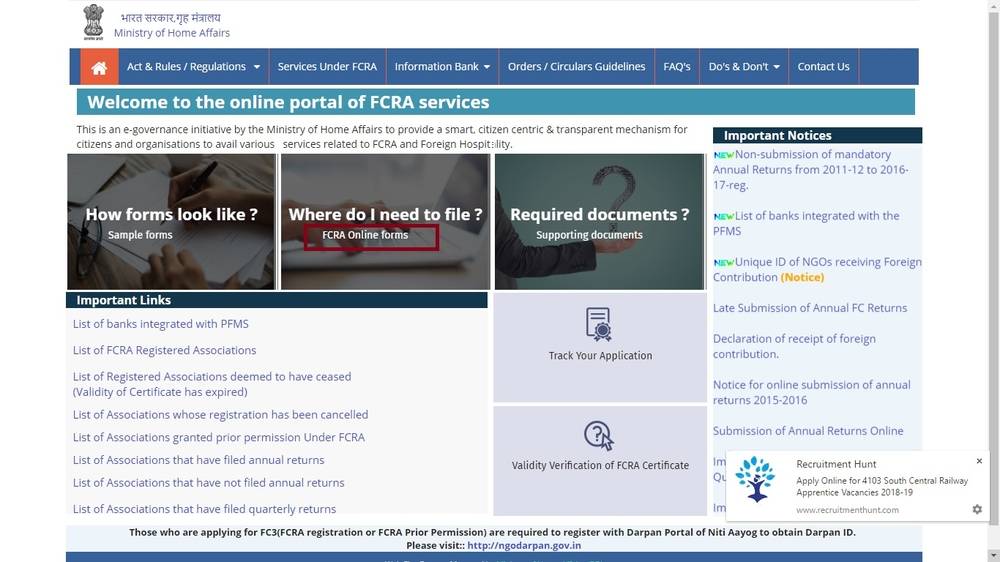

Step 1: Go to FCRA online portal. Step 2: Click on ‘FCRA online forms’ to register in FCRA. Image 1 Fcra Registration For Trusts And Ngos

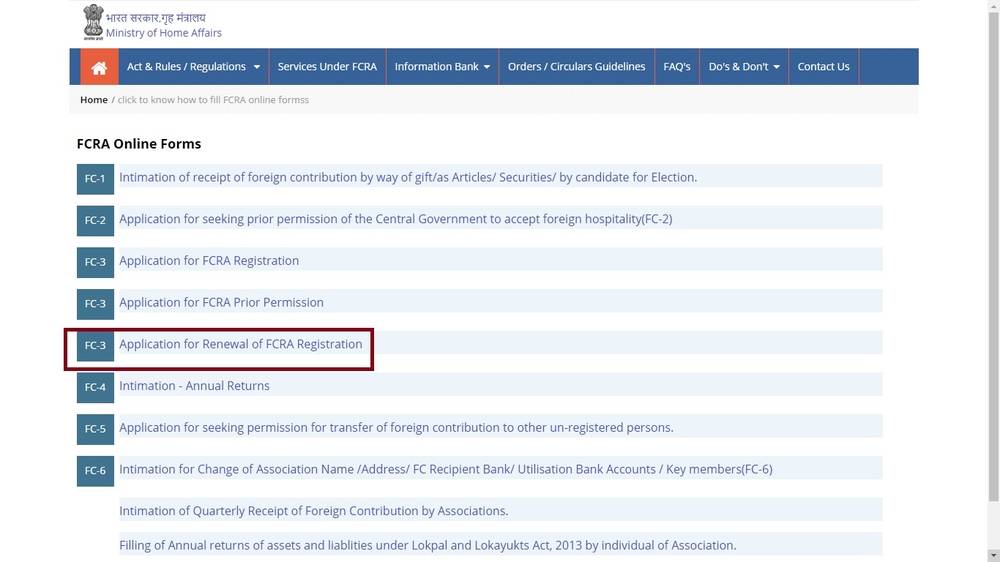

Step 3: In the next screen select application for FCRA registration link. The link will redirect to next page.

Image 1 Fcra Registration For Trusts And Ngos

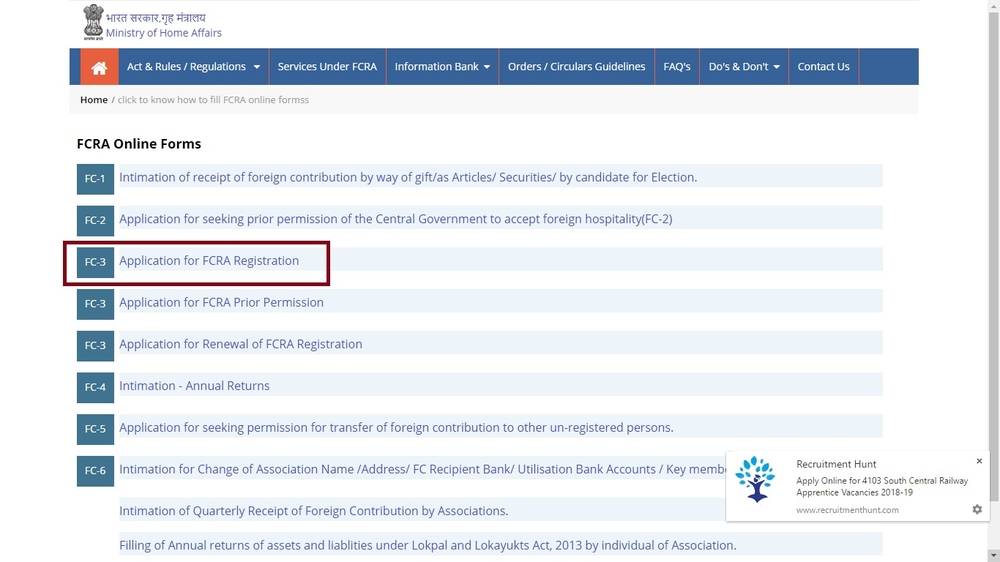

Step 3: In the next screen select application for FCRA registration link. The link will redirect to next page.

Image 2 Fcra Registration For Trusts And Ngos

Step 4: Click on 'Click to apply online' button to apply for FC3 (Registration).

Image 2 Fcra Registration For Trusts And Ngos

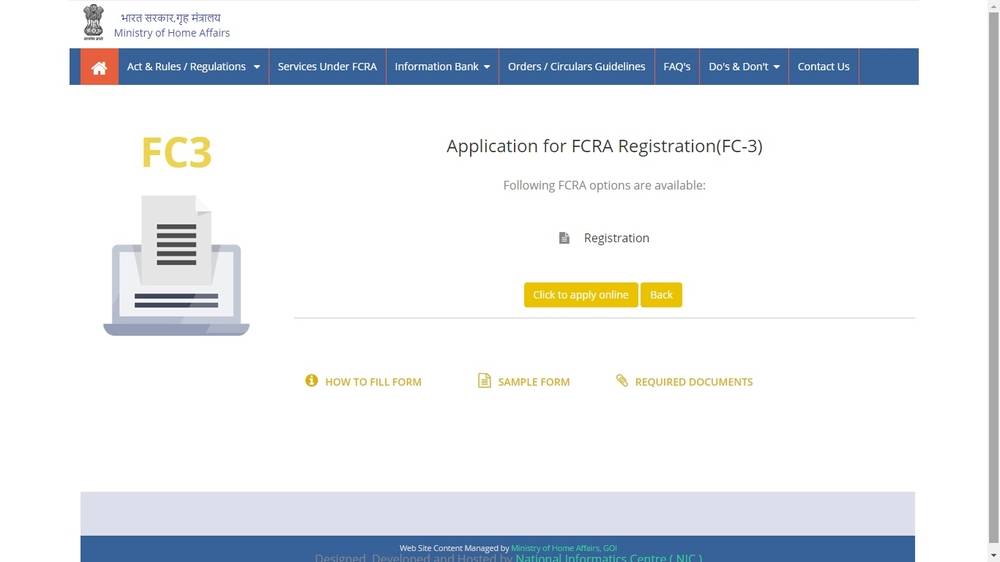

Step 4: Click on 'Click to apply online' button to apply for FC3 (Registration).

Image 3 Fcra Registration For Trusts And Ngos

Sign up for FCRA Account

Step 5: You need to sign up into FCRA, select sign-up option. The link will move to next page.

Image 3 Fcra Registration For Trusts And Ngos

Sign up for FCRA Account

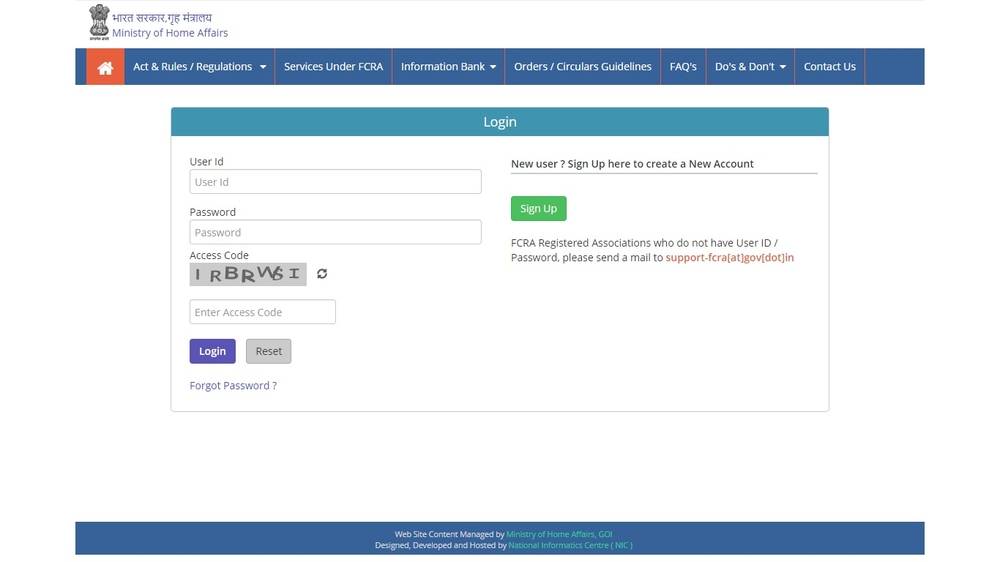

Step 5: You need to sign up into FCRA, select sign-up option. The link will move to next page.

Image 4 Fcra Registration For Trusts And Ngos

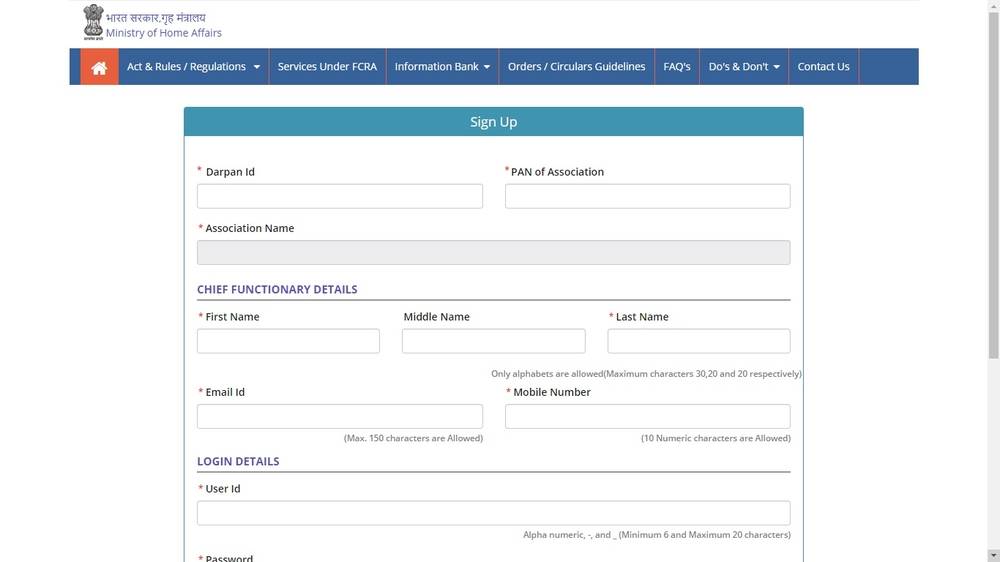

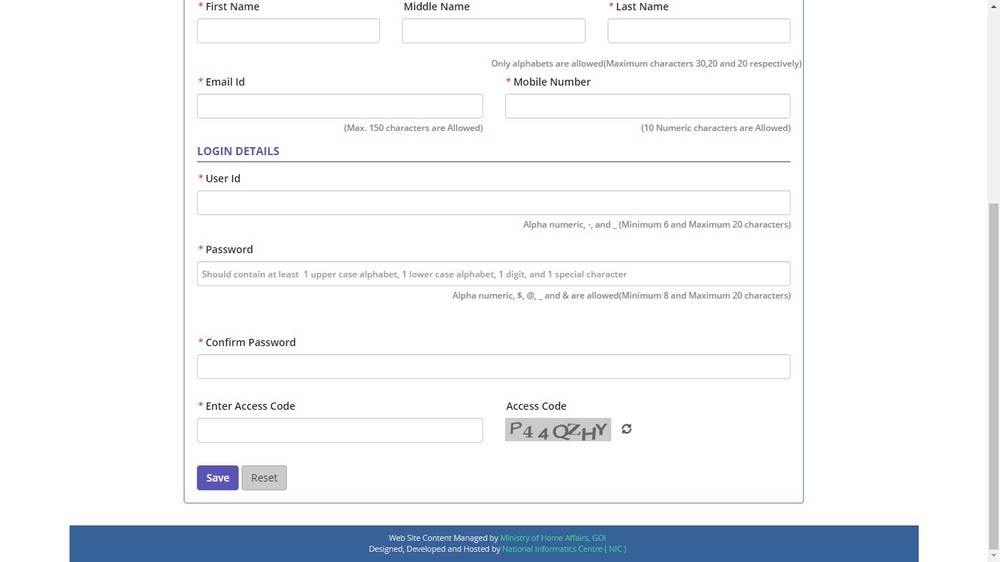

Step 6: Enter all mandatory details and click on save.

Image 4 Fcra Registration For Trusts And Ngos

Step 6: Enter all mandatory details and click on save.

Image 5 Fcra Registration For Trusts And Ngos

Image 5 Fcra Registration For Trusts And Ngos

Image 6 Fcra Registration For Trusts And Ngos

Step 7: On clicking on save a message will be shown in the screen ‘User ID successfully created and Your user ID is:’

Login to FCRA

Step 8: Login into the portal using this User ID and password.

Step 9: You can see an option ‘I am applying for’ select FCRA registration from drop-down menu. Click on Apply online.

Step 10: To proceed registration ‘click here to Proceed New Registration’

Step 11: Click on FC3 Menu in title bar for proceedings step by step registration.

Association Details

Step 12: Select Association Details from the menu. The association detail form will be displayed. Enter all below mentioned mandatory details.

Image 6 Fcra Registration For Trusts And Ngos

Step 7: On clicking on save a message will be shown in the screen ‘User ID successfully created and Your user ID is:’

Login to FCRA

Step 8: Login into the portal using this User ID and password.

Step 9: You can see an option ‘I am applying for’ select FCRA registration from drop-down menu. Click on Apply online.

Step 10: To proceed registration ‘click here to Proceed New Registration’

Step 11: Click on FC3 Menu in title bar for proceedings step by step registration.

Association Details

Step 12: Select Association Details from the menu. The association detail form will be displayed. Enter all below mentioned mandatory details.

- Darpan ID

- Address of Association

- Registration number

- Place of registration

- Date of registration

- Nature of association

- Main aim of the association

Renewal of FCRA Registration

Once FCRA registration is granted, it is valid for a period of five years. An application for renewal of FCRA registration can be made 6 months prior to the date of expiry, to keep the registration valid.

Step 1: Select Application for Renewal of FCRA Registration from FCRA Online Forms. Image 7 Fcra Registration For Trusts And Ngos

Step 2: On clicking on this, the page will be redirected to next page. Select Click to apply online.

Step 3: Enter your user ID & password and login to the FCRA portal.

Step 4: You can see an option ‘I am applying for’ select FCRA renewal from drop-down menu. For renewing FCRA registration follow above given steps 10 to 28.

Image 7 Fcra Registration For Trusts And Ngos

Step 2: On clicking on this, the page will be redirected to next page. Select Click to apply online.

Step 3: Enter your user ID & password and login to the FCRA portal.

Step 4: You can see an option ‘I am applying for’ select FCRA renewal from drop-down menu. For renewing FCRA registration follow above given steps 10 to 28.

To obtain FCRA Registration in India, get in touch with a Contact CA or IndiaFilings Business Advisor.