IndiaFilings

Expert

Published on: Jul 30, 2026

Calculating GST Payment Due - Electronic Liability Register

The GST platform in India uses a system of three ledgers, namely Electronic Liability Register, Electronic Credit Ledger, and

Electronic Cash Ledger. These ledgers provide support to manage the GST liability, credit, payment due, deposits, interest, penalty and late fee or any other debit/credit amount of each of the taxpayers. The electronic liability register maintained in FORM GST PMT-01 provide support to manage the GST payment due, interest, penalty, late fee as well as any other amount of a taxpayer. In this article, let us look at the procedure for calculating GST payment due to the Common Portal.Electronic Liability Register

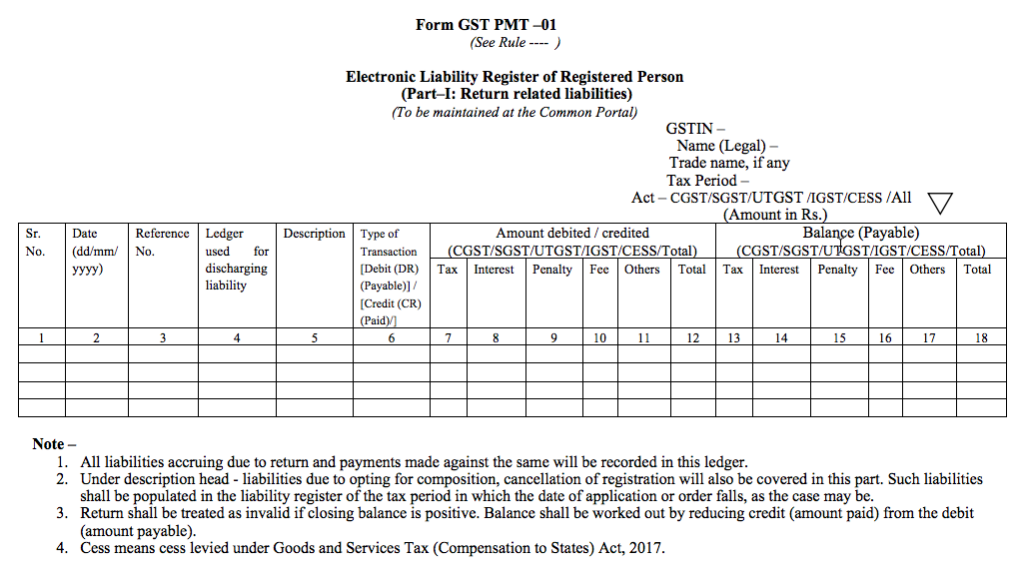

The taxpayer shall access the electronic liability register or GST PMT-01 through the GST Common Portal for any reference. The electronic liability register accounts for:

- The amount payable towards tax, interest, late fee or any other amount payable as per the return furnished by the taxpayer;

- Amount related to tax, interest, penalty or any other amount payable as determined by a proper officer in pursuance of any proceedings under the Act or as ascertained by the taxpayer;

- Amount of tax and interest payable as a result of mismatch under section 42 or section 43 or section 50; or

- Amount of interest that may accrue from time to time.

GST Form PMT-01 - Part A

GST Form PMT-01 - Part A

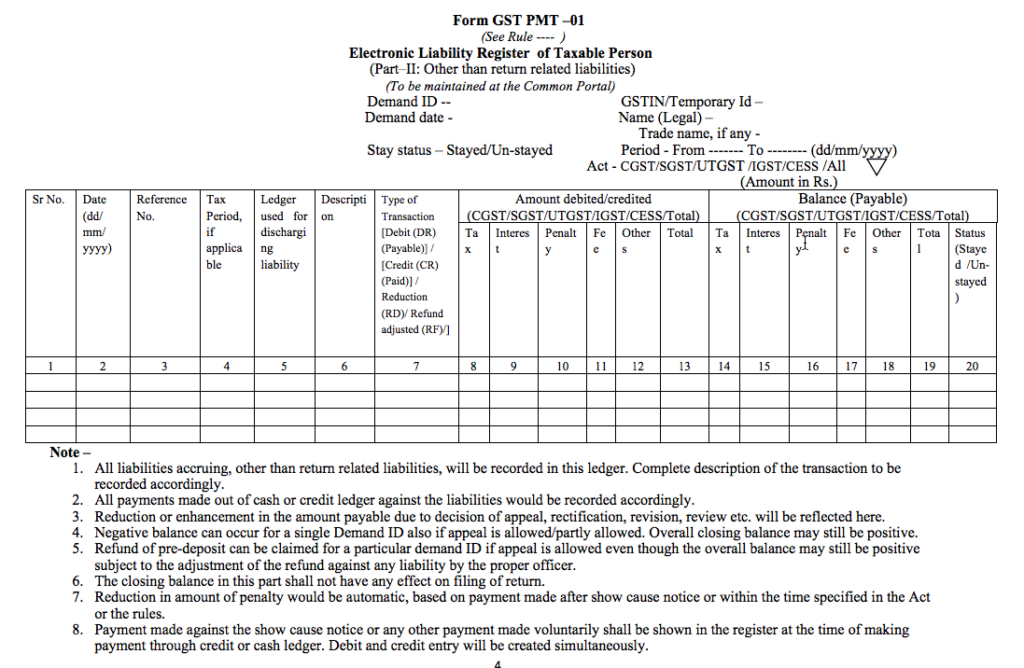

GST Form PMT-01 - Part B

The liability of a registered person as per his return is recorded by debiting the electronic credit ledger or the electronic cash ledger and the electronic liability register is credited accordingly.

The electronic cash ledger pays any amount deducted under section 51, or the amount collected under section 52, or the amount payable on a reverse charge basis, or the amount payable under section 10 any amount payable towards interest, penalty, fee or any other amount under the Act. Therefore the electronic liability registers credits accordingly.

For any amount of demand debited in the electronic liability, the register reduceds to the extent of relief given by the appellate authority or Appellate Tribunal or court and the electronic tax liability register would be credited accordingly. In case of an amount of penalty imposed or liable to be imposed would stand reduced partly or fully, as the case may be, if the taxpayer makes the payment of tax, interest and penalty specified in the show cause notice or demand order and the electronic liability register would be credited accordingly.

GST Form PMT-01 - Part B

The liability of a registered person as per his return is recorded by debiting the electronic credit ledger or the electronic cash ledger and the electronic liability register is credited accordingly.

The electronic cash ledger pays any amount deducted under section 51, or the amount collected under section 52, or the amount payable on a reverse charge basis, or the amount payable under section 10 any amount payable towards interest, penalty, fee or any other amount under the Act. Therefore the electronic liability registers credits accordingly.

For any amount of demand debited in the electronic liability, the register reduceds to the extent of relief given by the appellate authority or Appellate Tribunal or court and the electronic tax liability register would be credited accordingly. In case of an amount of penalty imposed or liable to be imposed would stand reduced partly or fully, as the case may be, if the taxpayer makes the payment of tax, interest and penalty specified in the show cause notice or demand order and the electronic liability register would be credited accordingly.

Calculating GST Payment Due

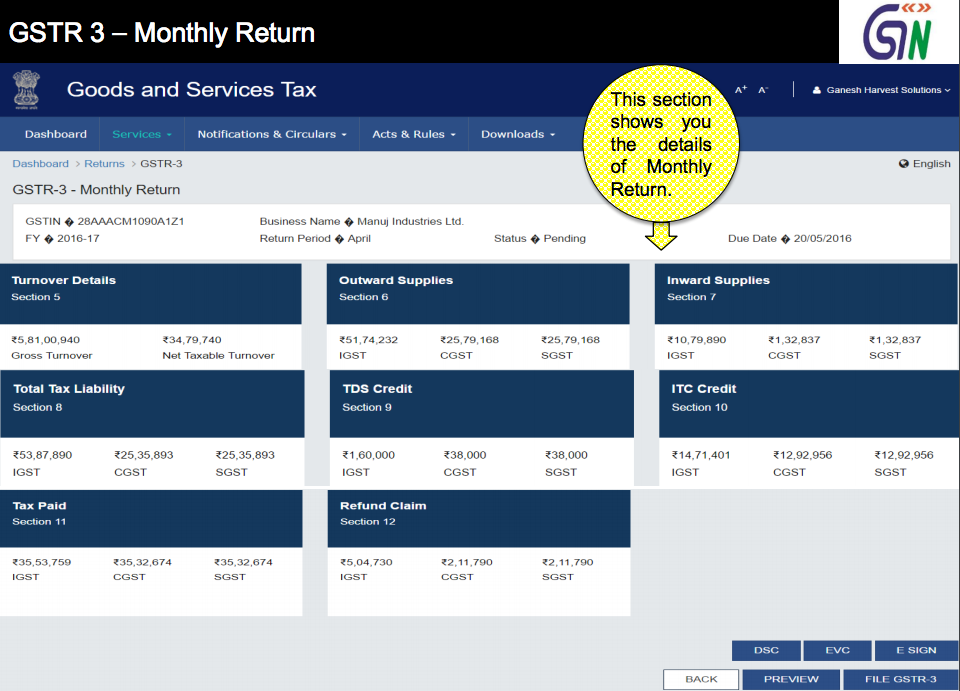

The GST payment due in any month can be readily viewed on the GST Common Platform dashboard after filing of GSTR-3, the

GST Monthly Return. GSTR-3 or Monthly Return is due on the 20th of each month. Prior to filing GSTR-3, the taxpayer must have filed GSTR-1 and GSTR-2 on the 10th and 15th of each month, respectively. Step 1: Access the GST Monthly Return or GSTR-3 Summary Page Access GSTR-3 Dashboard

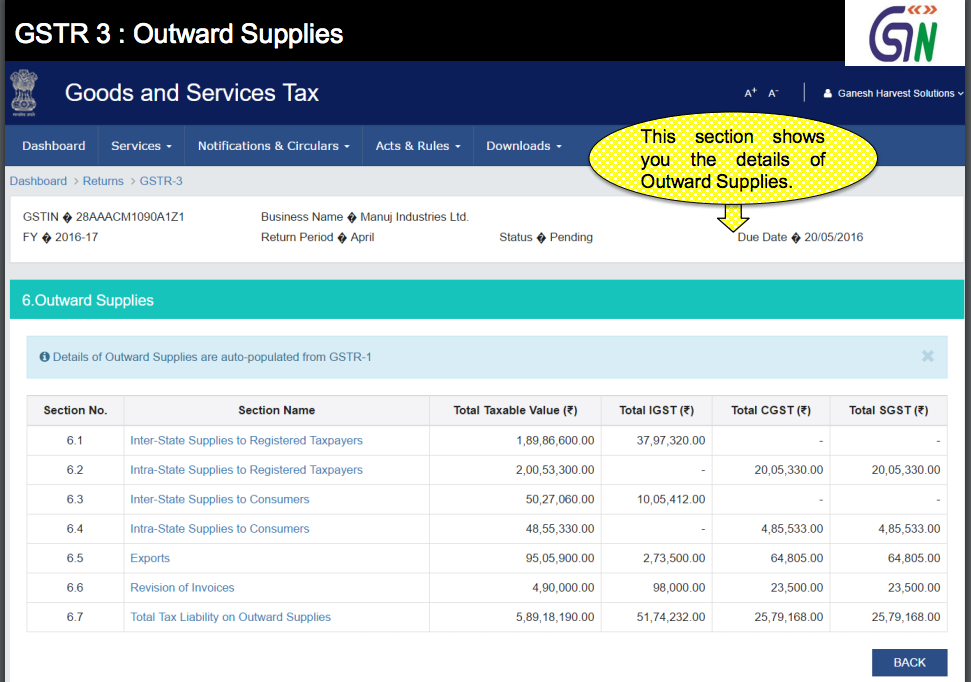

Step 2: The GSTR-3 Outward Supplies summary page displays all the outward supplies

Access GSTR-3 Dashboard

Step 2: The GSTR-3 Outward Supplies summary page displays all the outward supplies

GST Outward Supplies Summary

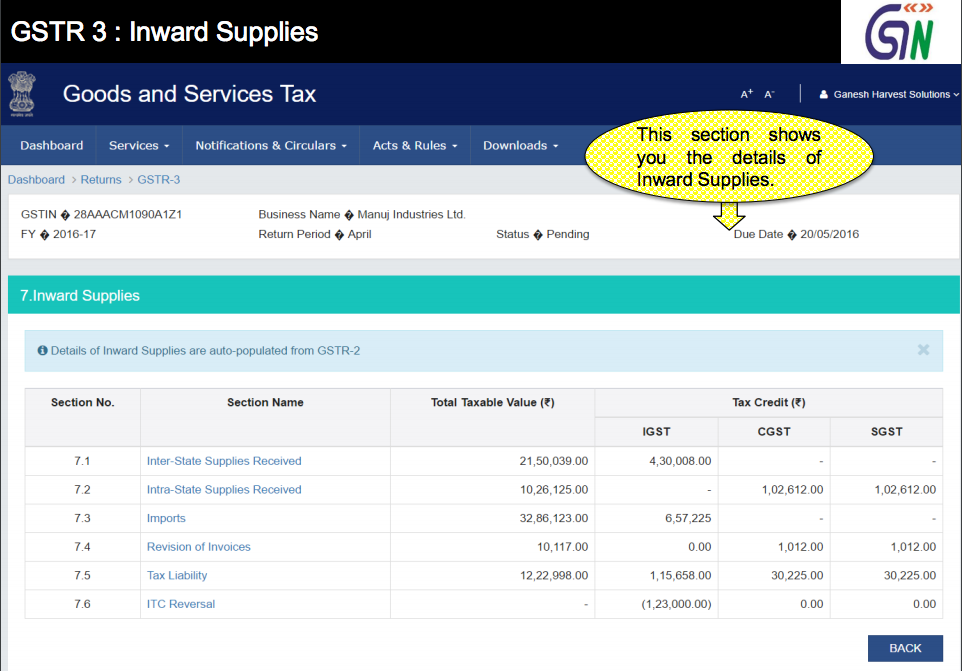

Step 3: The total tax credit or details or inward supplies can be viewed by accessing the GSTR-3 Inward Supplies Summary

GST Outward Supplies Summary

Step 3: The total tax credit or details or inward supplies can be viewed by accessing the GSTR-3 Inward Supplies Summary

GST Input Tax Credit Summary

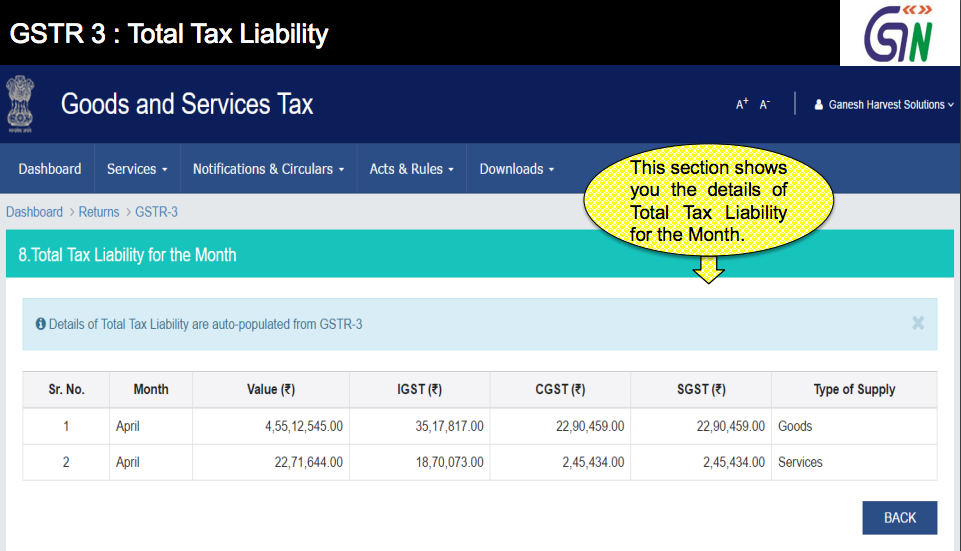

Step 4: View the total GST tax payment due

GST Input Tax Credit Summary

Step 4: View the total GST tax payment due

GST Total Liability

Simplify the GST registration & GST return filing process with IndiaFilings experts!

GST Total Liability

Simplify the GST registration & GST return filing process with IndiaFilings experts!