RENU SURESH

Expert

Published on: Jul 30, 2026

Simplified GST Registration Scheme (Rule 14A): Eligibility, Steps, and Process

To ease compliance and promote ease of doing business for small taxpayers, the Government of India has introduced a Simplified GST Registration Scheme under Rule 14A of the CGST Rules, 2017. Notified through Notification No. 18/2025 – Central Tax, effective from 1st November 2025, this scheme offers a fast-track, Aadhaar-authenticated GST registration process for businesses with limited monthly output tax liability. By enabling eligible applicants to obtain GST registration within three working days, the new rule aims to simplify the entry into the GST ecosystem, especially for small service providers and B2B suppliers with lower turnover. This article explains the eligibility criteria, step-by-step application process, and exit conditions under Rule 14A in a clear and practical manner.

Quick Summary

- What’s new: A new Rule 14A lets small taxpayers opt for a streamlined, fully electronic GST registration. Separately, Rule 9A enables system‑identified applicants to receive registration within 3 working days.

- Who can opt for Rule 14A: Applicants under Rule 8 who self‑assess that their monthly output tax liability on supplies made to registered persons won’t exceed ₹2.5 lakh.

- Aadhaar check: OTP‑based Aadhaar authentication is mandatory for the Primary Authorised Signatory and at least one Promoter/Partner (with limited exceptions notified under section 25(6D)).

- Approval timeline: Registration under Rule 14A is to be granted electronically within 3 working days after successful Aadhaar authentication.

- One registration per State/UT under Rule 14A: You cannot obtain another registration in the same State/UT under Rule 14A against the same PAN. (Regular registrations under other rules remain distinct.)

What is Rule 14A?

Rule 14A of the CGST Rules, 2017, introduces an optional, simplified registration route for applicants who file under Rule 8 and whose self‑assessed output tax liability on B2B supplies (supplies made to registered persons) stays within ₹2.5 lakh per month. It is designed to fast‑track onboarding while preserving standard GST obligations.Related change: New Rule 9A allows the portal to auto‑grant registration to certain applicants within 3 working days based on data analysis and risk parameters—separate from Rule 14A’s “opt‑in” track.

Who is Eligible?

You can consider Rule 14A if all the following apply:

- Application filed under Rule 8 (i.e., a standard GST registration route).

- You determine that your monthly output tax liability on supplies to registered persons (including CGST, SGST/UTGST, IGST, and Compensation Cess) does not exceed ₹2.5 lakh.

- You (other than categories notified under section 25(6D)) complete OTP‑based Aadhaar authentication for the Primary Authorised Signatory and one Promoter/Partner.

- You are not seeking another Rule 14A registration in the same State/UT against the same PAN.

How to Apply on the GST Portal (Rule 14A)

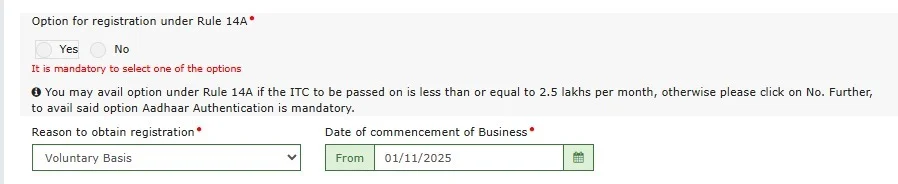

- Start Form GST REG‑01 (Rule 8) as usual.

- In Part B of REG‑01, select “YES” for “Option for registration under rule 14A” and tick the accompanying declaration.

- Complete OTP‑based Aadhaar authentication for the Primary Authorised Signatory and one Promoter/Partner.

- On successful authentication, the portal grants registration electronically within 3 working days from submission.

Note: Rule 14A modifies registration forms (REG‑01/02/03/04/05) and introduces REG‑32 (Withdrawal application) and REG‑33 (Order on withdrawal) to support the scheme operationally.

Conditions to Remember (once registered under Rule 14A)

- Portal constraint: While you remain under Rule 14A, the system is configured around the ₹2.5 lakh/month B2B output‑tax limit noted above. If you need to go beyond, first withdraw from Rule 14A (see below).

- No duplicate Rule 14A registration in the same state/UT for the same PAN.

- Standard GST duties continue: Rule 14A changes how you register, not tax rates or the existence of returns. You must continue to comply with applicable return and payment obligations as a regular taxpayer (subject to any government notifications that may separately modify forms/timelines).

Simple examples

Example 1 — Service provider (18% GST):

Riya invoices ₹12,00,000 in a typical month to registered clients.Approx GST on those B2B invoices = ₹2,16,000 (12,00,000 × 18%).Since ₹2.16 lakh ≤ ₹2.5 lakh, Riya can opt for Rule 14A.

Example 2—Trader with mixed buyers:

Aman sells ₹30 lakh/month total. To registered buyers he sells ₹14 lakh at 18% → GST ≈ ₹2.52 lakh. Since ₹2.52 lakh > ₹2.5 lakh, he should not opt for Rule 14A. (He can still apply for normal registration; Rule 14A is optional.)

Tip: The ₹2.5 lakh check is about GST amount, not turnover. If your items have different rates, total up the tax on your B2B invoices for a typical month.

How to Exit (Withdraw) from Rule 14A later

If you outgrow the threshold or simply want to move out of Rule 14A, follow this structured process:

Before you apply to withdraw (REG‑32), make sure:

- All returns from your effective date of registration up to the withdrawal application date are filed, and

- If applying before 1 Apr 2026 → you’ve filed at least 3 months of returns; or

- If applying on/after 1 Apr 2026 → at least 1 tax period of returns; and

- No amendment/cancellation application is pending; no Section 29 cancellation proceedings have been started/are pending.

Filing & Effect

- File REG‑32 online. The officer verifies; the order is issued in REG‑33 (or rejected in REG‑05).

- Once withdrawal is allowed, you can report B2B GST above ₹2.5 lakh from the 1st day of the month after the order month.

- You cannot go back and amend earlier months to cross the limit. (Back‑dating isn’t permitted.)

Filing and outcome

- File FORM GST REG‑32 online (Aadhaar authentication/biometrics may be prompted).

- Your application is verified under Rule 9; the officer issues an order in FORM GST REG‑33 (allow) or REG‑05 (reject) within the Rule 9 timeline.

- If allowed, you can furnish output tax liability exceeding the Rule 14A limit from the first day of the succeeding month in which the withdrawal order is issued. You cannot retrospectively amend prior periods to exceed the limit.

- If cancellation proceedings (Section 29) start after you file a withdrawal, the withdrawal application is rejected and deemed approval safeguards won’t apply.

Rule 14A vs Rule 9A: What’s the difference?

- Rule 14A (you opt‑in): For applicants under Rule 8 who self‑assess a B2B output‑tax liability ≤ ₹2.5 lakh/month; registration is granted within 3 working days post Aadhaar authentication, and certain portal/form constraints apply until you withdraw.

- Rule 9A (system‑identified): Irrespective of Rule 14A, any applicant under Rule 8/12/17 can be auto‑approved electronically within 3 working days if flagged by the system as per risk analytics.

Common Mistakes to Avoid

- Checking the wrong box: Don’t forget to select “Yes” for Rule 14A in REG‑01 if you want the simplified route.

- Guessing the limit: Estimate your monthly B2B GST carefully—use your prices and applicable rates.

- Skipping Aadhaar: Keep Aadhaar and the linked mobile ready; any mismatch slows down approval.

- Late withdrawal: If you’re about to cross the limit, file REG‑32 early. You can’t backdate higher liability.

How IndiaFilings can help

- Eligibility check & advisory: We’ll review your turnover profile and B2B output‑tax exposure to confirm Rule 14A suitability.

- End‑to‑end registration: Preparing REG‑01, guiding Aadhaar authentication, and tracking the 3‑day electronic grant.

- Compliance setup: Return calendar, e‑invoicing/e‑way bill readiness (as applicable), and alerts to avoid threshold breaches.

- Seamless exit (if needed): We’ll handle REG‑32/REG‑33 and ensure all preconditions are met for a smooth transition out of Rule 14A.

Let IndiaFilings check your eligibility and file your application—fast, accurate, and fully compliant.

Related Guides:

GST Registration in 3 Days: Detailed Rules & Requirements

GST Registration in 3 Days: Step-by-Step Procedure

GST Registration within 3 Days: India’s New Auto-Approval System to Begin Nov. 1, 2025