RENU SURESH

Expert

Published on: Jul 30, 2026

GST Registration in 3 Days: Detailed Rules & Requirements – 2025 Updates

In a move to simplify the GST registration process, the Central Board of Indirect Taxes and Customs (CBIC) introduced the Central Goods and Services Tax (Fourth Amendment) Rules, 2025, via Notification No. 18/2025 – Central Tax on October 31, 2025, which took effect on November 1, 2025. These changes primarily aim to ease the compliance burden for businesses, especially smaller taxpayers, by streamlining processes and introducing electronic systems for faster registration and withdrawal.This article provides a comprehensive overview of the key amendments, highlighting their implications for businesses and taxpayers.

Key Highlights of the Amendment

Here’s a detailed explanation of the new rules and how they will impact businesses across India:

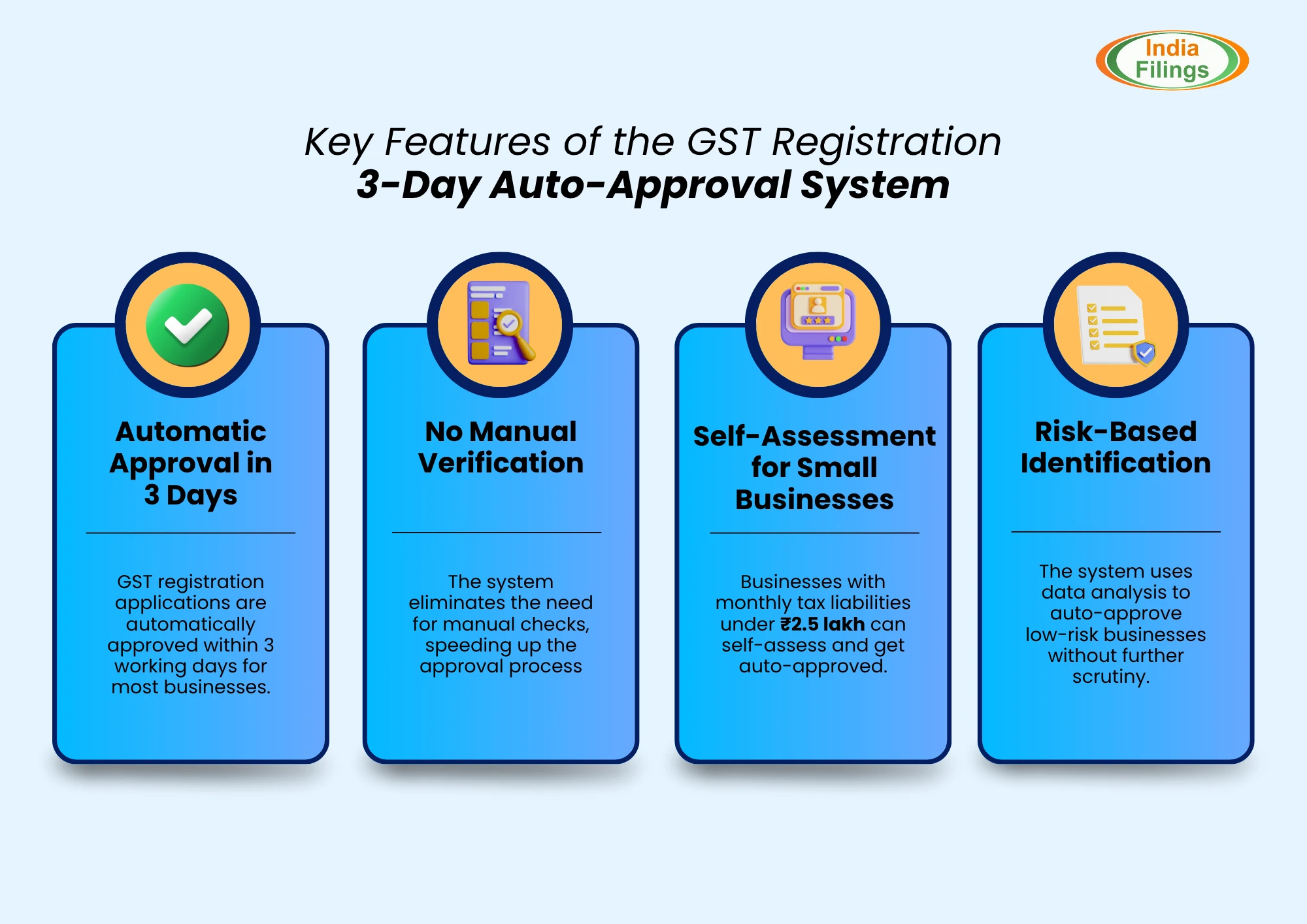

Electronic Grant of GST Registration within 3 Working Days (Rule 9A)

A major shift is the introduction of Rule 9A, which ensures the electronic grant of GST registration within 3 working days for taxpayers applying through the common portal. This is applicable to those applying for registration under Rules 8, 12, or 17. What does this mean for taxpayers?

- The GST registration process has become faster, as registration will be granted based on data analysis and risk parameters identified by the system, reducing the need for lengthy verification processes.

- This will be particularly beneficial for businesses and individuals who need to register quickly, without unnecessary delays.

Simplified Registration for Small Taxpayers (Rule 14A)

Under the new provisions of Rule 14A, businesses with a monthly output tax liability below ₹2.5 lakh have the option to register electronically. This new rule introduces a simplified procedure aimed at reducing the compliance burden for small taxpayers. Key conditions under Rule 14A:

- The applicant must not have a monthly tax liability exceeding ₹2.5 lakh.

- Aadhaar authentication is mandatory for successful registration under this rule.

- Once registered under this provision, businesses are eligible to withdraw from the option if their tax liability exceeds the threshold. However, there are certain conditions for withdrawal, including the submission of tax returns and no ongoing cancellation proceedings.

Click here to know more about the Simplified GST Registration Scheme (Rule 14A)

Introduction of New Forms for Registration and Withdrawal

The amendment introduces several new forms to facilitate the new registration and withdrawal provisions:

- GST REG-32 (Application for Withdrawal): This form allows taxpayers to request the withdrawal of their registration under Rule 14A.

- GST REG-33 (Order of Withdrawal): This form is used by the tax authority to approve or reject a withdrawal application.

Additionally, existing forms like GST REG-01 (Application for Registration), GST REG-02 (Acknowledgment), and others have been revised to reflect the changes in the registration and withdrawal process.

Risk-Based Verification and Data Analysis

A significant feature of the new amendments is the reliance on risk parameters and data analysis to speed up the GST registration process. This means that registration is now based on an automated system that evaluates risk and verifies data before granting approval. As a result, the need for manual intervention has been reduced, ensuring a quicker and more efficient registration process.

Also Read: GST Registration within 3 Days: India’s New Auto-Approval System to Begin Nov. 1, 2025

Conditions for Withdrawal from the GST Registration Option

The amendment introduces a clear process for withdrawing from the electronic registration option under Rule 14A:

- A taxpayer can apply for withdrawal by filing GST REG-32, but must ensure that all returns for the period from the date of registration to the withdrawal application date are filed.

- The Aadhaar authentication process must be completed before filing for withdrawal.

- If there are no ongoing cancellation proceedings, the application will be processed and either accepted or rejected within a stipulated timeframe.

Amendment to Existing Registration Forms

Several existing registration forms have been updated to reflect these changes:

- Form GST REG-01 now includes an option to declare if the taxpayer is applying under Rule 14A.

- Form GST REG-02 acknowledges the registration application and confirms whether it is for the new electronic process under Rule 14A.

- Forms GST REG-03 and GST REG-04 have been revised to address the updated verification and clarification requirements under the new rules.

Benefits of the New Amendments

The new GST registration amendments bring several advantages, including faster registration, simplified processes for small businesses, and streamlined ITC management.

- Faster Processing: With Rule 9A, businesses can now receive their GST registration within 3 working days. This change eliminates long waiting periods and promotes faster business operations.

- Simplification for Small Businesses: The introduction of Rule 14A offers a simple, electronic registration option for small businesses with a low tax liability. This reduces compliance costs and administrative hurdles for smaller players.

- Aadhaar Authentication: Mandatory Aadhaar authentication ensures that businesses are easily verified, promoting transparency and trust in the system.

- Clear Process for Withdrawal: The new forms and detailed withdrawal process under Rule 14A provide a clear and structured approach for businesses that no longer wish to remain under the simplified GST registration option.

- Risk-Based Approach: By using data analysis and risk parameters, the new system ensures that only genuine businesses are granted registration, reducing the chances of fraud and errors.

What Businesses Need to Do Now

To take advantage of the new 3-day GST registration process, businesses must ensure they meet the eligibility criteria, complete Aadhaar authentication, and file all necessary returns to comply with the updated rules. Here's what you need to do to get started.

- Stay Updated: If your business is small with output tax liabilities under ₹2.5 lakh per month, consider opting for the simplified electronic registration option under Rule 14A.

- File Returns on Time: If you plan to withdraw from the simplified registration process, make sure all returns are up to date and meet the requirements for withdrawal.

- Ensure Aadhaar Authentication: Aadhaar authentication is mandatory for both registration and withdrawal applications under the new rules.

- Prepare for Changes in GSTIN: Keep track of any GSTIN changes and understand how ITC reversal will be handled to avoid complications.

Conclusion

The Central Goods and Services Tax (Fourth Amendment) Rules, 2025 are a major step towards simplifying the GST registration process. With the electronic registration system now being faster and more efficient, small businesses stand to benefit the most. These changes not only streamline registration but also provide businesses with the flexibility to manage their operations better as they grow.

Get Your GST Registration Easily with IndiaFilings

Are you looking to register your business for GST and take advantage of the new 3-day auto-approval system? IndiaFilings can help you with hassle-free GST registration and ensure you stay compliant with the latest regulations.

Contact IndiaFilings today for quick and easy GST registration!

Related Guides

GST Registration in 3 Days: Step-by-Step Procedure

Simplified GST Registration Scheme (Rule 14A): Eligibility, Steps, and Exit Process

GST Registration within 3 Days: India’s New Auto-Approval System to Begin Nov. 1, 2025