IndiaFilings

Expert

Published on: Apr 22, 2026

Basics of Transfer Pricing in India

The transaction between two companies belonging to the same group in different will not be subject to the same market forces that affect the transaction between two independent companies. For instance, the price at which a good or service is transferred from a subsidiary company to a holding company would be arbitrary and dictated by the Management. Whereas, the price at which a good or service is transferred between two independent companies would be market-determined, subject to competition. Under or overvaluation of transactions happening between two entities of the same group could lead to revenue loss for the Government. Hence, the concept of transfer pricing has been implemented to ensure all commercial transactions between different entities of a multinational group are transacted at an arms-length price.

Need for Transfer Pricing

The following illustrations provide the basis for the implementation of transfer pricing framework: Illustration: Scenario Without Transfer Pricing

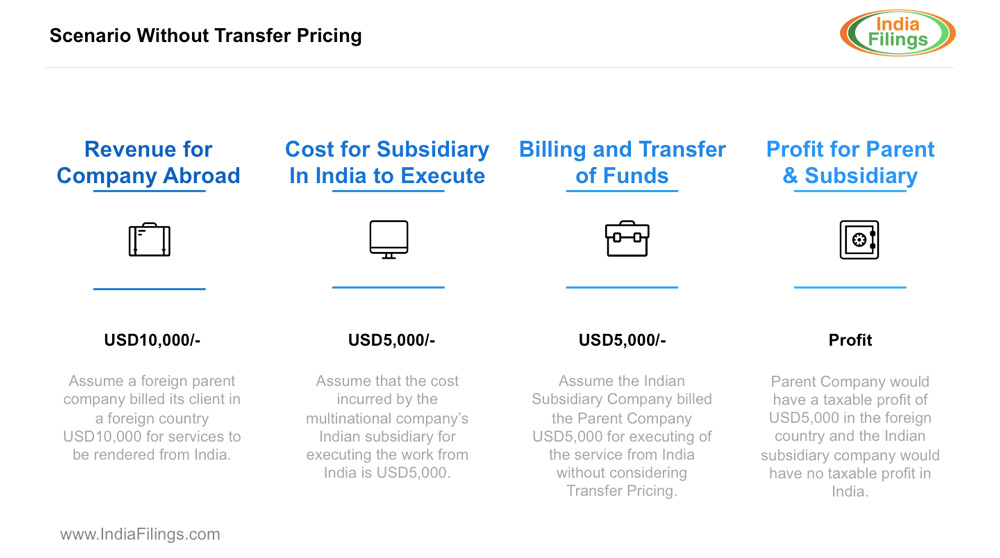

Illustration: Scenario Without Transfer Pricing

In the above scenario without transfer pricing, the parent company abroad would pay taxes on USD5000, whereas the Indian subsidiary company would pay no taxes. Hence, a scenario without transfer pricing mechanism could lead to revenue loss and also a drain on foreign exchange reserves.

Illustration: Scenario with Transfer Pricing

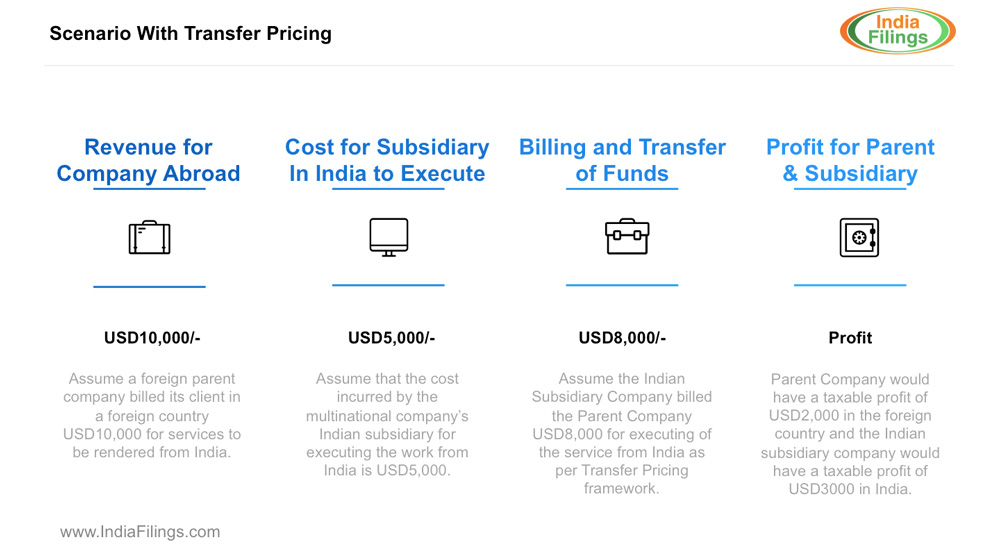

Illustration: Scenario with Transfer Pricing

As illustrated above, in a scenario with transfer pricing mechanism, both countries would have taxable revenues when the services are transferred at arms-length pricing.

What is an Associated Enterprise?

An Associated Enterprise is any enterprise that participates directly or indirectly or through one or more intermediaries in the management or control or another enterprise as per the Income Tax Act. If an enterprise holds shares having 26% or more voting power in the other enterprise, then it shall be considered an Associated Enterprise. Thus, the term includes enterprises under common ownership, management or control.

When is transfer pricing regulations applicable?

When there is an international transaction between two associated enterprises, transfer pricing regulations are applicable. The transaction covered under transfer pricing regulation includes purchase, sale or lease of tangible or intangible property, provision of services, lending or borrowing of money, cost-sharing arrangement or any other transaction, which has a bearing on the profits, income, losses or assets of an Enterprise.

When such a transaction occurs between associated enterprises, the income arising from the transaction should be computed having regard to the arm's length price.

What is arm's length price?

Arm's length price is the price at which independent parties charge under uncontrolled conditions. An uncontrolled condition is a transaction taking place between two independent parties under free market forces. Therefore, the international transaction between two associated enterprises must take place at arm's length price.

How to determine the arm's length price?

The following are some of the accepted methodologies for calculating arm's length price:

- Comparable Uncontrolled Price Method

- Resale Price Method

- Cost Plus Method

- Profit Split Method

- Transactional Net Margin Method

- Other methods as prescribed by the CBDT

Maintaining Record of Transfer Pricing

Every entity entering into an international transaction with an associated enterprise is required to keep and maintain documents and information pertaining to the transaction. Further, entities entering into international transaction during a previous year are required to obtain a report from an accountant and file it along with the income tax return.

To start or manage a business in India, visit IndiaFilings.com