Marlin Priya

Expert

Published on: Mar 28, 2026

West Bengal Professional Tax

Professional tax is a State Government tax levied on the income received by employment, profession, calling, or trade. The Municipal Corporations of the respective states impose professional tax through predetermined slab rates. Professional tax is paid on a monthly or annual basis. Moreover, it can be claimed as a deduction from the salary under Section 16 of the Income Tax Act. Different states cover different rates and methods of collection for professional tax. This article looks at the details of West Bengal professional tax and its e-payment procedure. To learn more about Professional Tax Registration and Compliance, Click here.Eligibility

The West Bengal State Legislature passed the “West Bengal State Tax on Professions, Trades, Callings and Employments Act, 1979” for its citizens. The persons liable to pay Profession Tax under the Act are divided into two categories.- In the case of salaried persons and wage earners, the employer (Public and Private Sectors, Government who distribute salary or wages to the employees) deducts the Profession Tax from the salary or wages and is liable to deposit the same with the State Government.

- For other categories of individuals, the person who has engaged in employment, profession, calling, and trade is responsible for paying the tax.

Exemption from West Bengal Professional Tax

The State Government may exempt or reduce the payable tax for any class of persons by issuing notifications. Currently, the members of the forces and the members of the Indian Navy serving in any part of West Bengal are exempted from the payment of professional tax. The exemption also applies to any person drawing a pay or an allowance in Army or Air Force, or Navy. The members of auxiliary forces or reservists serving in any part of West Bengal and drawing pay and allowances as additional forces or reservists are exempted from payment of Profession Tax.Salary and Wages

Any person earning a salary or wages is liable to pay professional tax. Salary and wages under the West Bengal State Tax on Professions, Trades, Callings and Employments Act, 1979 are described below. Salary and wages include the following.- Pay, Dearness Allowance, and any other amount paid as allowance.

- Remunerations are received in cash or any other kind regularly.

- Honorarium, perquisites, and profit instead of salary

- Leave encashment amount

- Leave concessional pay and subsistence allowance.

- Medical reimbursement

- Reimbursement of conveyance charges, traveling allowance

- Salary paid to apprentice under Apprentices Act, stipend paid to the trainee

- Statutory bonus, gratuity, and ex-gratia payment.

- Pension granted to an employee is not considered a salary. Therefore, pensioners are not liable to pay Professional Tax on their retirement.

Requisites for West Bengal Professional Tax Payment

The self-employed person requires the Certificate of Enrolment and receipt of annual tax payment but does not require filing any return. An Employer requires a Certificate of Registration, monthly tax payment, and annual returns filing.West Bengal Professional Tax Slab Rate

The ‘Schedule’ of tax rates per West Bengal State Tax on Professions, Trades, Callings, and Employments Act, 1979, is provided in the table. The professional tax should be paid at the rates specified in the West Bengal Professional Tax Schedule.| S. No | Class of persons / Income | Rate of tax |

| 1) | Employees earning monthly salary or wages— (i) Not exceeding Rs.8,500 (ii) Above Rs.8,500 but not exceeding Rs. 10,000 (iii) Above Rs. 10,000 but not exceeding Rs. 15,000 (iv) Above Rs. 15,000 but not exceeding Rs. 25,000 (v) Above Rs.25,000 but not exceeding Rs.40,000 (vi) Above Rs.40,000 | Nil, Nil* Rs.110 per month Rs. 130 per month Rs. 150 per month Rs. 200 per month |

| 2) | The annual gross income in the preceding year or part thereof of any persons engaged in any profession or calling but not employed as an employee is – (i) Not more than Rs. 60,000 (ii) Above Rs. 60,000 but not exceeding Rs. 72,000 (iii) Above Rs. 72,000 but not exceeding Rs. 84,000 (iv) Above Rs. 84,000 but not exceeding Rs. 96,000 (v) Above Rs. 96,000 but not exceeding Rs. 1,08,000 (vi) Above Rs. 1,08,000 but not exceeding Rs. 1,80,000 (vii) Above Rs. 1,80,000 but not exceeding Rs. 3,00,000 (viii) Above Rs. 3,00,000 but not exceeding Rs. 5,00,000 (ix) Above Rs. 5,00,000 | Nil Rs. 480 per annum Rs. 540 per annum Rs. 600 per annum Rs. 1,080 per annum Rs. 1,320 per annum Rs. 1,560 per annum Rs. 2,000 per annum Rs. 2,500 per annum |

| 3) | The annual gross turnover or gross yearly receipt in the preceding year or part thereof of any persons engaged in any profession or trade that involves the supply of goods or services or both is— (i) Not more than Rs. 5,00,000 (ii) Above Rs. 5,00,000 but not exceeding Rs.7,50,000 (iii) Above Rs. 7,50,000 but not exceeding Rs.25,00,000 (iv) Above Rs. 25,00,000 but not exceeding Rs. 50,00,000 (v) Above Rs. 50,00,000 | Nil Rs. 300 per annum Rs. 600 per annum Rs. 1,200 per annum Rs. 2,500 per annum |

| 4) | Persons engaged in any profession, trade, or calling in West Bengal. | Rs. 2,500 per annum |

Enrollment

Every person who comes under entry numbers 2 to 4 of the “Schedule” attached to the Act should acquire an Enrolment Certificate within 90 days from the date of liability to pay tax. A person liable to pay tax should apply for enrolment. The concerned Deputy Commissioner / Profession Tax Officer will notify and determine the tax to be paid by an enrolled person if they fail to pay the due tax or pay less than the actual amount to be paid. If a person fails to apply for enrolment within the prescribed days, a penalty of Rs.100 will be imposed for delay of each month or part of it. Besides, the provision of punishment with simple imprisonment with or without a fine is available for the said default.Registration

Every employer (not being a Government officer) should apply and secure a Certificate of Registration to deduct the professional tax from the salary or wages payable to his employees. The tax must be removed per the slab mentioned in Serial No.1 of the Schedule. Such an employer should apply for registration online within 90 days from the date of liability. An employer with more than one work within the jurisdiction of different authorities should make a separate application for registration. However, the Commissioner of Profession Tax may allow single registration for the whole of West Bengal. An employer failing to apply for registration within 90 days from the date of liability will be imposed a penalty of Rs 500 for the delay of each month or part of it.Professional Tax Return Filing

All registered employers are required to submit the returns, wherein an enrolled person is not required to file any returns. For late filing of Return, a late fee of Rs 200/- must be paid for the first month of default and Rs 100/- for each subsequent month. Non-submission of Return is a punishable offense with simple imprisonment with or without a fine.Due Date for Professional Tax Payment

Profession Tax can only be paid through the Government of West Bengal online portal.- The enrolled persons should pay the professional tax on or before July 31st of each financial year.

- For registered employers, professional tax should be paid monthly.

West Bengal Professional Tax e-Payment

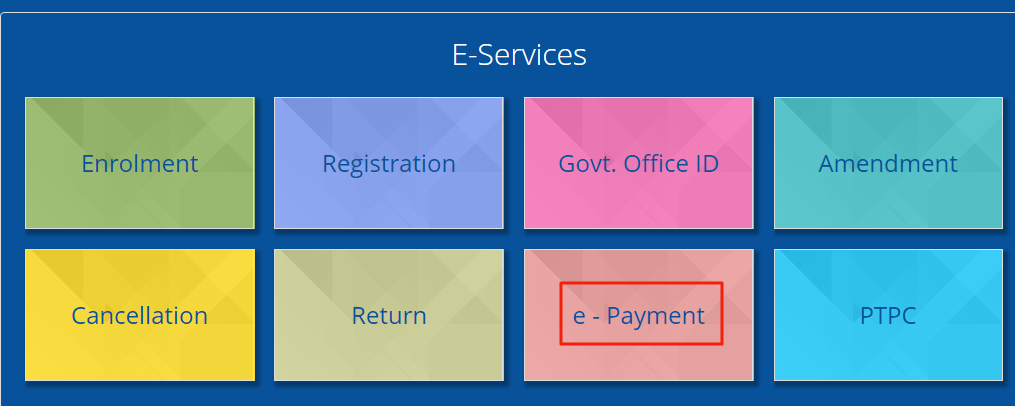

The Directorate of Commercial Taxes under the Government of West Bengal facilitates the e-payment of Profession Tax for its citizens. Step 1: To pay professional tax online, visit the official website of the West Bengal professional tax online portal. Step 2: The home page appears. Under the e-Services menu, click the e-Payment tab redirecting to another page. West Bengal Professional Tax

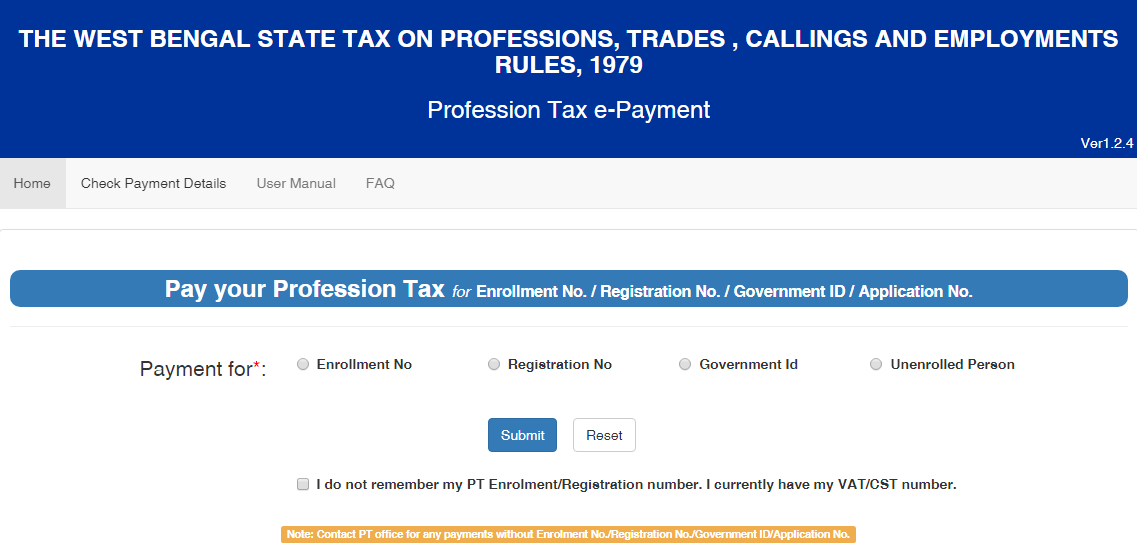

Step 3: The e-Payment can be made through 4 options.

West Bengal Professional Tax

Step 3: The e-Payment can be made through 4 options.

- Using Profession Tax Enrolment No (12-digit numeric)

- Using Profession Tax Registration No (12-digit numeric)

- Using Profession Tax Government ID (12-digit numeric)

- Using Application No for new Profession Tax Enrolment (11-digit numeric)

West Bengal Professional Tax- e-Payment

West Bengal Professional Tax- e-Payment

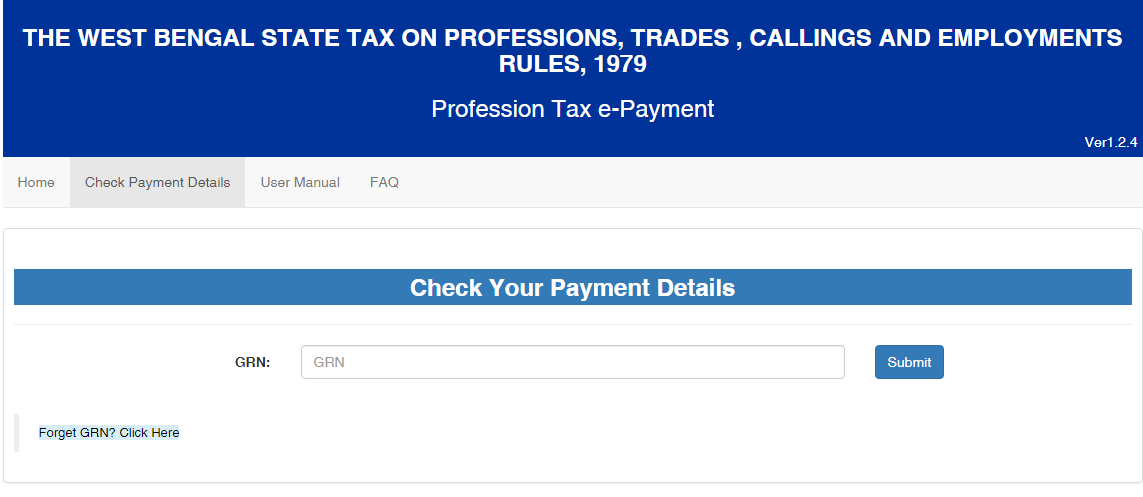

Check Payment Details

The status of the payment made can be checked by entering the Government Receipt number (GRN), and clicking submit. West Bengal Professional Tax- Check Payment Details

West Bengal Professional Tax- Check Payment Details

Penalties

The Profession Tax Act provides for the imposition of penalties in different cases. Some such cases are: -- Willful failure to apply for enrolment /registration within the prescribed time.

- They are intentionally providing false information in the application for registration/enrolment.

- Failure to file the Return within the prescribed time.

- Failure to pay tax within the prescribed time.

- Willful failure to maintain books of accounts and records.

Prosecution

The West Bengal Profession Tax law provides for prosecution for certain offenses. Such offenses are bailable with simple imprisonment, fine, or both. The violations include:-- Failure to pay tax by an enrolled person.

- Failure to furnish a return by a registered employer.

- We are furnishing incorrect information in Return.

- Refusal or negligence to provide information as required under the law.

- Failure to produce and explain records and books of accounts for inspection as required by an authority under the law.