IndiaFilings.com

Expert

Published on: Jul 30, 2026

Rule 114b And Form 60 Filing For Income Tax

Rule 114B of the Income Tax Rules, 1962 require mandatory quoting of PAN in respect of certain transactions for capturing information pertaining to high-value transactions and curbing black money circulation. In this article, we look at Rule 114B of the Income Tax Rules in detail along with the form which should be used for Form 60 filing.Transactions Requiring PAN - Rule 114B

As per Rule 114B of the Income Tax Rules, any person or entity undertaking the following transactions are required to mandatorily quote their PAN in all the documents pertaining to the transaction.

- Sale or purchase of a motor vehicle or vehicle, which requires registration by a registering authority and other than two-wheeled vehicles

- Opening an account (other than a time-deposit or a basic savings bank deposit account) with a banking company or a co-operative bank

- Making an application to any banking company or a co-operative bank or to any other company or institution for the issue of a credit card or debit card.

- Opening of a Demat account with a depository-participant, custodian of securities or any other person registered the Securities and Exchange Board of India Act, 1992

- Cash payment of over Rs.50,000 to a hotel or restaurant against a bill or bills at any one time

- Cash payment of over Rs.50,000 for travel to any foreign country or payment for the purchase of any foreign currency at any one time

- Payment of over Rs.50,000 to a Mutual Fund for purchase of its units

- Payment of over Rs.50,000 to a company or an institution for acquiring debentures or bonds

- Payment of over Rs.50,000 to the Reserve Bank of India constituted under section 3 of the Reserve Bank of India Act, 1934 for acquiring debentures or bonds

- Deposit in cash of over Rs.50,000 with a banking company or a co-operative bank

- Purchase of bank drafts or pay orders or banker’s cheques from a banking company or a co-operative bank with a cash payment of over Rs.50,000 in a single day

- Deposit of amount exceeding Rs.50,000 or aggregating to more than Rs.5,00,000 during a financial year with a banking company or a co-operative bank

- Payment of over Rs.50,000 in a financial year for one or more pre-paid payment instruments to a banking company or a co-operative bank

- Payment of over Rs.50,000 as life insurance premium to an insurer

- Payment of over Rs.1 lakhs for a contract for sale or purchase of securities

- Sale or purchase of any immovable property with any payment of over Rs.10 lakhs

- Sale or purchase, by any person, of goods or services in a transaction over Rs.2 lakhs

In case a minor is undertaking the transaction, the PAN of the parent or guardian can be quoted. If a person does not have PAN, then PAN should be obtained or Form 60 must be filed.

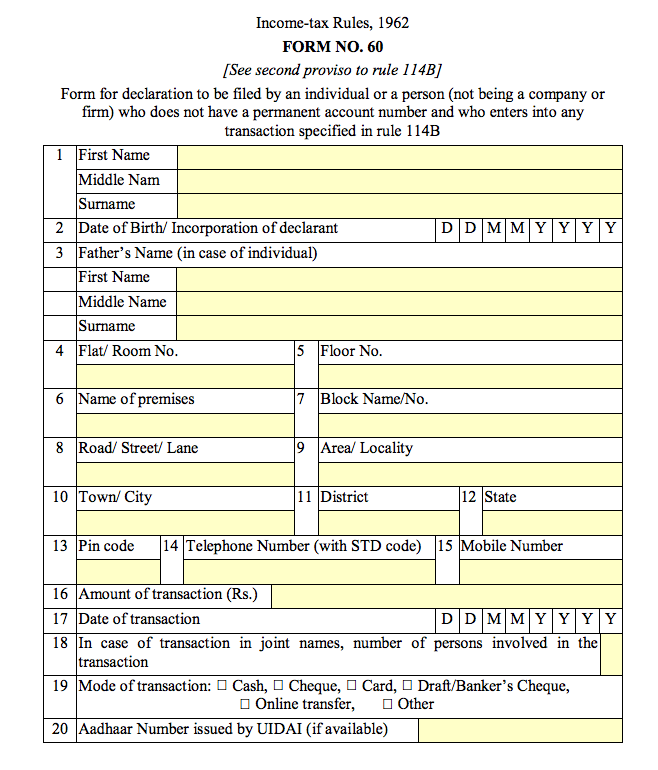

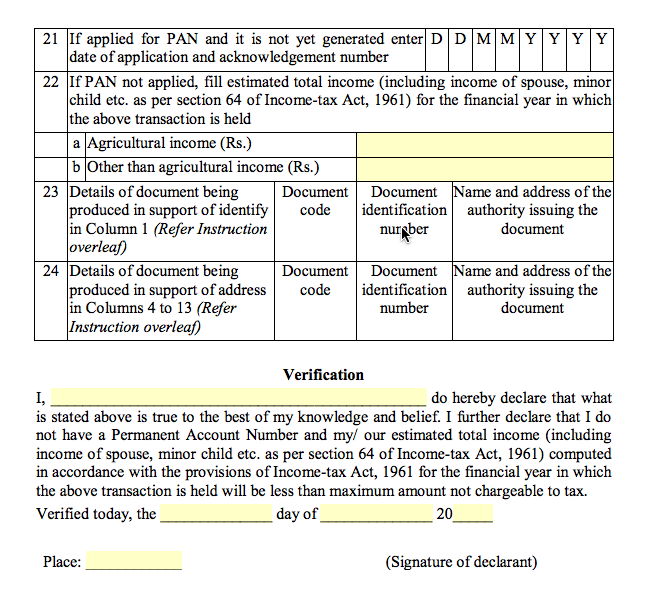

Filing Form 60

Form 60 is a declaration to be

filed by an individual or a person (not being a company or firm) who does not have a PAN and who enters into any transaction specified in rule 114B. Before signing Form 60 declaration, the declarant should satisfy himself that the information furnished in this form is true, correct and complete in all respects. Any person making a false statement in the declaration shall be liable to prosecution under section 277 of the Income-tax Act, 1961 and on conviction be punishable as under:- In a case where tax sought to be evaded exceeds twenty-five lakh rupees, with rigorous imprisonment which shall not be less than six months but which may extend to seven years and with fine;

- In any other case, with rigorous imprisonment which shall not be less than three months but which may extend to two years and with a fine.

Form 60 Income Tax - Page 1

Form 60 Income Tax - Page 1

Form 60 Income Tax - Page 2

To know about Advance Tax liability, click here.

Form 60 Income Tax - Page 2

To know about Advance Tax liability, click here.