Renu Suresh

Expert

Published on: Jun 24, 2026

Patents (Amendment) Rules, 2021

Ministry of Commerce and Industry has further amended the Patents Rules, 2003 in a notification dated September 23, 2021, to be called Patents (Amendment) Rules, 2021. The Amendment is brought under Rule 7 which prescribes the fees for grant of patents to applicants. The category of applicants for patent has been amended to specifically include "educational institution" along with a natural person, startup, and small entity. This is released in Gazette as per the requirement of the Government of India and the present article briefly explains the amendments undertaken vide the Patents (Amendment) Rules, 2021. Click here to know more about Intellectual Property Laws in IndiaSynopsis of Patents (Amendment) Rules, 2021

The Ministry of Commerce and Industry vide Patents (2nd Amendment) Rules, 2020, has reduced the statutory fee applicable for Startups and small entities for patent filing and prosecution. Now, in their recent amendment dated 21st September 2021, the Department for Promotion of Industry and Internal Trade published the Patents (Amendment) Rules, 2021 wherein educational institutions have also been added to the list of Natural Person, Start-ups, and Small Entities, to promote the creation, innovation, and development of new technologies in the educational sector. The union government has reduced the fee for patent filing and prosecution for educational institutions by 80%.Rule 7 of Patents Rules - Fee for patent filing

Rule 7 of Patents Rules, 2003 prescribes the fees payable under section 142 for the grant of patents. The Amendment is brought under Rule 7 which prescribes the fees for grant of patents to startup or small entity.- To obtain the Patent, the startup/entity/educational institution needs to pay the fee as per the fee scale specified in the First schedule of Rule 7 of Patents Rules, 2003. The first schedule species the fees payable under section 142 to issue patents and for which fees are required to be payable.

- The Startup/Small Entity/Educational institution need to pay a 10% additional fee when the applications for patent and other documents are filed through physical mode (in hard copy format)

- As per rule 7, the small entity needs to submit every document accompanied by Form-28, for which a fee has been specified.

The Patent Filing fee for Educational Institution

- Educational institutions engage in many research activities, where professors and teachers, and students generate several new technologies which need to be patented for facilitating commercialization of the same.

- At the time of applying for patents, the innovators have to apply for these patents in the name of the institutions which have to pay fees for large applicants, which are very high and thus work as a disincentive.

- In this regard and to encourage greater participation of the educational institutions, official fees payable by them in respect of various acts under the Patents Rules, 2003, have been reduced by way of the Patents (Amendment) Rules, 2021.

- Benefits related to 80% reduced fee for patent filing & prosecution have been extended to all educational institutions irrespective of them being Government-owned/ aided or private universities.

Highlights of Patents (Amendment) Rules, 2021

The amendments made in the Patents (Amendment) Rules, 2021 are summarized hereunder:Addition of Explanation for the Educational Institution

Under the new rules, an Educational Institution has been defined under Rule 2(ca) as follows: “a university established or incorporated by or under Central Act, a Provincial Act, or a State Act, and includes any other educational institution as recognized by an authority designated by the Central Government or the State Government or the Union territories in this regard;”.Addition of the term “educational institution in Rule 7 (1) and Form 28

The term “educational institution” has been inserted into the Rules by way of the second proviso to Rule 7 (1) and to Form 28. Provided further that in the case of a small entity, or startup, or educational institution, every document for which a fee has been specified shall be accompanied by Form-28. The new format of form 28 is attached here for reference:Substitution of Provisions Relating to the Payment of Patent Fee

The Amendment is brought under Rule 7 of Patents Rules, 2003 which prescribes the fees for grant of patents in which sub-rule 3 has been substituted as follows: If the patent application processed by a natural person or startup or small entity or educational institution is fully or partly transferred to a person other than a natural person, startup, or small entity or educational institution, the difference in the scale of fees needs to be paid by the new applicant with the transfer request. This rule is applicable in the following two cases:- The fees charged from the natural person, startup, or small entity

- The fees are chargeable from the person other than a natural person, startup, or small entity

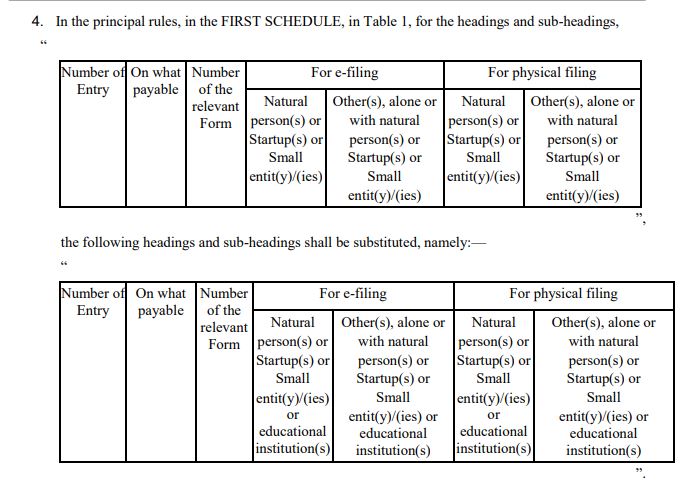

Amendment in Table I of the First Schedule of Patents Rules, 2003

Note: Fees once paid in respect of any proceeding will not ordinarily be refunded irrespective of whether the proceeding has taken place or not

Amendment in Table I of the First Schedule of Patents Rules, 2003

Note: Fees once paid in respect of any proceeding will not ordinarily be refunded irrespective of whether the proceeding has taken place or not

Earlier Amendments

The Patents Rules have consistently been amended in 2016, 2017, 2019, and 2020 to achieve the objective of removing procedural inconsistencies and unnecessary hurdles in the processing of applications thereby accelerating grant/registration and final disposal. Thus, the amendments have resulted in the following initiatives taken by the DPIIT:- Augmentation of manpower by recruiting new examiners.

- Simplified process of applying and granting patents completely through e-filing.

- Seamless Patent Hearings through Video conferencing for facilitating speedy and contact-less proceedings.

- Scheme for Facilitating Start-ups Intellectual Property Protection (SIPP)has been launched to provide facilitators to start-ups for filing and processing of their applications. Professional charges of such facilitators are reimbursed under the SIPP scheme.