RENU SURESH

Expert

Published on: Jun 24, 2026

Income Tax Slabs and Rates for FY 2025-26 (AY 2026-27)

Income tax rates play a crucial role in determining the tax liability of individuals and businesses, influencing financial planning and compliance. These rates vary based on income levels, taxpayer categories, and applicable tax slabs, ensuring a progressive taxation system. Understanding the current Income Tax Rates is essential for effective budgeting, tax-saving investments, and adherence to legal requirements. This article provides a comprehensive overview of the Income tax slab rates and taxable income bracket applicable for the Assessment Year 2025-2026 (Financial Year 2024-2025).

Income Tax Slab for 2025 - individuals (including resident senior citizen and resident super senior citizen) opting for old tax regime-

Here is the income tax slab for individuals applicable to Assessment Year 2025-26

| Individual (resident/ non-resident) below 60 years | Resident senior citizen (60 years or more but less than 80 years) | Resident super senior citizen above 80 years | |||

| Net Income | Tax Rates | Net Income | Tax Rates | Net Income | Tax Rates |

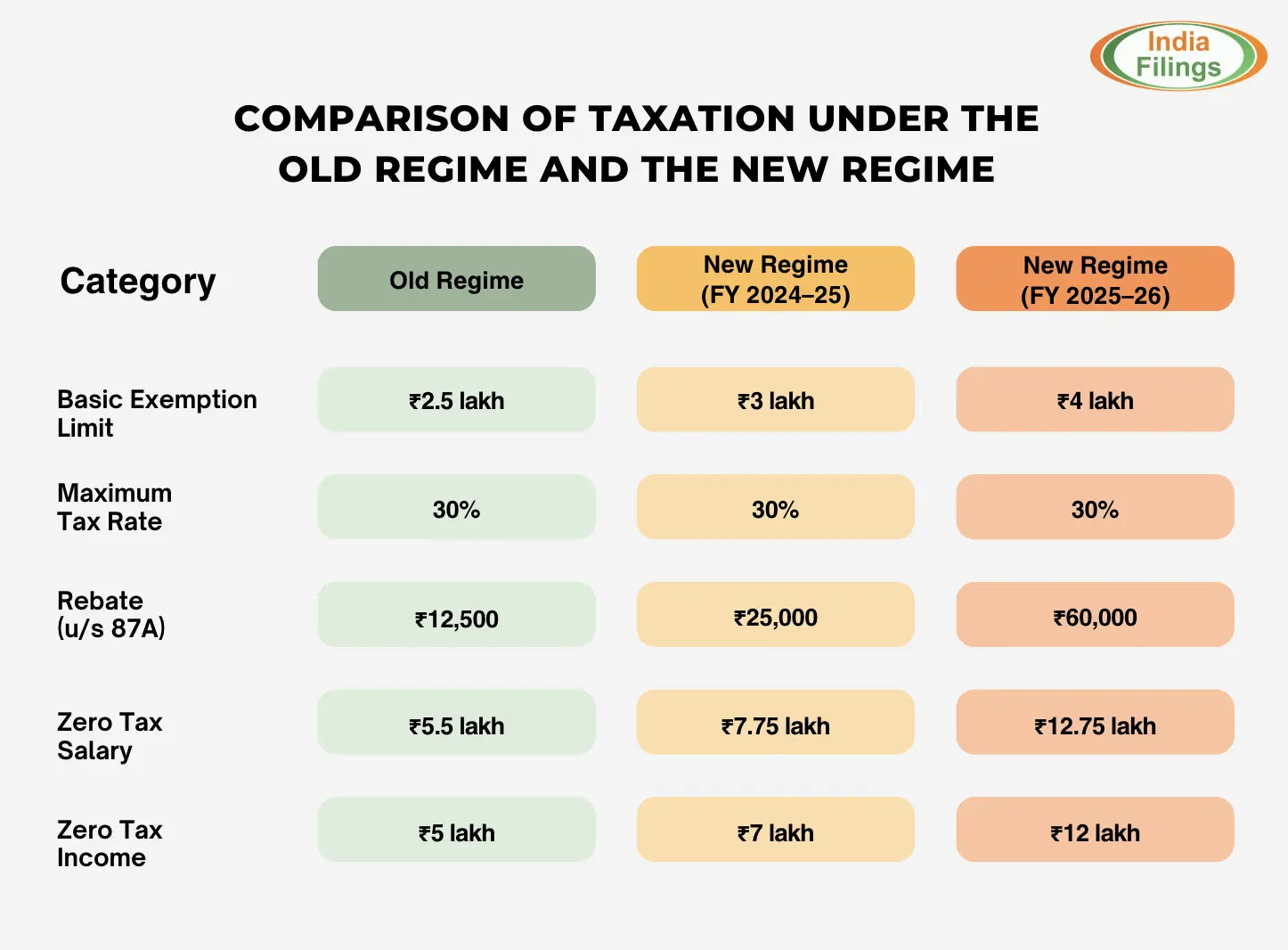

| Up to INR 2,50,000 | NIL | Up to INR 3,00,000 | NIL | Up to INR 5,00,000 | Nil |

| INR 2,50,001 to INR 5,00,000 | 5% | INR 3,00,001 to INR 5,00,000 | 5% | INR 5,00,001 to INR 10,00,000 | 20% |

| INR 5,00,001 to INR 10,00,000 | 20% | INR 5,00,001 to INR 10,00,000 | 20% | Above INR 10,00,000 | 30% |

| Above INR 10,00,000 | 30% | Above INR 10,00,000 | 30% | - | - |

Other points-

- Surcharge-

Surcharge is leviable at following rates on the amount of taxable income bracket -

| Particulars | Surcharge rates |

| Total income exceeds INR 50 Lakhs | 10% of the income tax |

| Total income exceeds INR 1 Crore | 15% of the income tax |

| Total income exceeds INR 2 Crores | 25% of the income tax |

| Total income exceeds INR 5 crores | 37% of the income tax |

- Health and Education Cess-

Health and Education Cess is leviable @4% on the amount of income tax + surcharge.

- Rebate under section 87A-

Rebate under section 87A is available to resident individual having total income less than INR 5 Lakhs. Lower of the following amounts is available as rebate-

- 100% of the income tax; or

- INR 12,500.

Income Tax Slab for 2025 - HUF/ AOP/ BOI/ any other artificial juridical person opting for old tax regime-

The following is the tax slab 2025 for HUF/AOP/BOI or any other juridical person option for old tax regime

| Net Income | Tax Rates |

| Up to INR 2,50,000 | NIL |

| INR 2,50,001 to INR 5,00,000 | 5% |

| INR 5,00,001 to INR 10,00,000 | 20% |

| Above INR 10,00,000 | 30% |

Other points-

- Surcharge-

Surcharge is leviable at following rates on the amount of income tax-

| Particulars | Surcharge rates |

| Total income exceeds INR 50 Lakhs | 10% of the income tax |

| Total income exceeds INR 1 Crore | 15% of the income tax |

| Total income exceeds INR 2 Crores | 25% of the income tax |

| Total income exceeds INR 5 crores | 37% of the income tax |

- Health and Education Cess-

Health and Education Cess is leviable @4% on the amount of income tax + surcharge.

New Income Tax Slab for 2025 - Individual and HUF opting for new tax regime (section 115BAC)-

We have given below the tax slab 2025 for individuals and HUF opting for the new tax regime.

| Total Income | Tax Rates |

| Up to INR 2,50,000 | NIL |

| INR 2,50,001 to INR 5,00,000 | 5% |

| INR 5,00,001 to INR 7,50,000 | 10% |

| INR 7,50,001 to INR 10,00,000 | 15% |

| INR 10,00,001 to INR 12,50,000 | 20% |

| INR 12,50,001 to INR 15,00,000 | 25% |

| Above INR 15,00,000 | 30% |

Other points-

- Surcharge-

Surcharge is leviable at following rates on the amount of income tax as per tax slab 2025-

| Particulars | Surcharge rates |

| Total income exceeds INR 50 Lakhs | 10% of the income tax |

| Total income exceeds INR 1 Crore | 15% of the income tax |

| Total income exceeds INR 2 Crores | 25% of the income tax |

| Total income exceeds INR 5 crores | 37% of the income tax |

- Health and Education Cess-

Health and Education Cess is leviable @4% on the amount of income tax + surcharge.

- As per the new regime, the benefit of lower rates are available only if the total income is calculated without claiming specified exemptions or deductions.

New Income Tax Slab for 2025 - partnership firm (including LLP)-

Here is the tax slab 2025 for partnership firm (including LLP),

| Particulars | Corresponding Rates |

| Rates of Income tax | 30% |

| Surcharge applicable when total income exceeds INR 1 Crore | 12% of the amount of income tax |

| Health and Education Cess | 4% of the amount of income tax + surcharge. |

Income tax slab for 2025 - domestic company (normal rates and special rates)-

Normal Rates-

| Particulars | Rates as per Tax slab 2025 |

| Company having turnover/ gross recipients up to INR 400 Crores in the previous year 2019-2020 | 25% |

| Any other domestic company | 30% |

- Surcharge-

Surcharge is leviable at following rates on the amount of income tax-

| Range of Total Income | Surcharge rates |

| INR 1 Crore to INR 10 Crores | 7% of the income tax |

| Above INR 10 Crores | 12% of the income tax |

- Health and Education Cess-

Health and Education Cess is leviable @4% on the amount of income tax + surcharge.

Special Rates-

| Particulars | Rates |

| Domestic Company opting under section 115BA | 25% |

| Domestic Company opting under section 115BAA | 22% |

| Domestic Company opting under section 115BAB | 15% |

- Surcharge-

Surcharge is leviable at following rates on the amount of income tax-

| Particulars | Surcharge rates |

| Domestic company opting under section 115BAA | 10% of the income tax (irrespective of the amount of total income) |

| Domestic company opting under section 115BAB | 10% of the income tax (irrespective of the amount of total income) |

- Health and Education Cess-

Health and Education Cess is leviable @4% on the amount of income tax + surcharge.

- Applicability of MAT-

Domestic company opting under section 115BAA and section 115BAB is exempted from the provisions of MAT. Accordingly, MAT provisions are applicable to domestic company opting under section 115BA.

New Income Tax Slab for 2025 - foreign company-

Here is the taxable income bracket 2025 for foreign company,

| Particulars | Corresponding Rates |

| Rates of Income tax | 40% |

| Surcharge | · 2% for total income ranging between INR 1 Crore to INR 10 Crores. · 5% for total income ranging above INR 10 Crores. |

| Health and Education Cess | 4% of the amount of income tax + surcharge. |

New Income Tax Slab AY 2025-26 for Co-operative society-

| Income | Rates |

| Up to INR 10,000 | 10% |

| INR 10,001 to INR 20,000 | 20% |

| Above INR 20,000 | 30% |

- Surcharge-

Surcharge is leviable at the rates of 12% only when the total income exceeds INR 1 Crore.

- Health and Education Cess-

Health and Education Cess is leviable @4% on the amount of income tax + surcharge.

- Rates for co-operative society opting under section 115BAD-

| Particulars | Corresponding Rates |

| Rates of Income tax | 22% |

| Surcharge | 10% of the amount of income tax |

| Health and Education Cess | 4% of the amount of income tax + surcharge |

New Income Tax Slab AY 2025-26 for local authority-

| Particulars | Corresponding Rates |

| Rates of Income tax | 30% |

| Surcharge | 12% of the amount of income tax when the total income exceeds INR 1 Crore. |

| Health and Education Cess | 4% of the amount of income tax + surcharge |

Latest Update

Pay Later Option for Income Tax Filing

The Income Tax e-filing portal has recently rolled out a 'Pay Later' option, allowing you to complete your tax filing process before making any tax payments. You can pay taxes after you are done filing. For additional information, please refer to our guide –Tax Filing GuidePay later option for the Income tax return filing.Extension of Due Date for Filing ITR

The due date of ITR filing for FY 2024-25 (AY 2025-26) has been extended to 15th September 2025 from 31st July 2025.

File Your Income Tax with Ease — Powered by IndiaFilings

Don't let tax season stress you out. Whether you're a salaried individual, freelancer, or business owner, IndiaFilings offers expert-assisted Income Tax Filing services to help you file accurately and on time. Our professionals ensure maximum deductions, zero penalties, and full compliance with the latest tax laws. Get started today and experience hassle-free filing — all from the comfort of your home!

Frequently Asked Questions (FAQs)

1. Can I claim deductions under Section 80C while opting for the new tax regime?

No. The new tax regime does not allow most deductions and exemptions available under the old regime. This includes deductions under Section 80C, which cannot be claimed if you opt for the new regime.

2. What is the rebate under Section 87A?

Section 87A offers a rebate to individual taxpayers with income below a certain threshold.

- Under the new tax regime, the rebate is applicable for income up to ₹7 lakh.

- Under the old regime, it applies to income up to ₹5 lakh.

If your income falls within these limits, your tax liability becomes zero.

3. What is the tax-free income limit in India?

Under the old tax regime:

- Individuals below 60 years: up to ₹2.5 lakh

- Senior citizens (60–79 years): up to ₹3 lakh

- Super senior citizens (80+ years): up to ₹5 lakh

Under the new tax regime: Basic exemption limit is ₹3 lakh for all individuals, regardless of age.

4. Is it mandatory to opt for the new tax regime for AY 2025–26?

No, taxpayers can choose between the old and new regimes. However, if you wish to continue with the old regime and claim deductions and exemptions, you must explicitly opt out of the new regime while filing your return. Otherwise, the new tax regime will apply by default.

5. Is the standard deduction allowed in the new tax regime?

Yes.

- Under the new regime (FY 2024–25): Standard deduction of ₹75,000

- Under the old regime: Standard deduction of ₹50,000

This deduction is available on salary income.

6. What deductions are allowed in the new tax regime?

Some specific deductions are permitted, including:

- ₹75,000 standard deduction on salary

- Interest on home loan for let-out property (Section 24b

- Employer’s contribution to NPS (Section 80CCD)

- Contributions to Agniveer Corpus Fund (Section 80CCH)

- Deduction on family pension (Lower of 1/3rd pension or ₹25,000)

7. Is HRA exemption available in the new tax regime?

No, House Rent Allowance (HRA) exemption under Section 10(13A) is not available under the new tax regime.

8. Has the new tax regime changed for FY 2024–25?

Yes. The new regime has been revised in Budget 2024 for FY 2024–25, including changes to slabs and deductions.

8. Can I save tax under the new tax regime?

Yes. Budget 2024 revisions allow taxpayers to save up to ₹17,500 by opting for the new regime due to more favourable tax slabs and higher standard deductions.

9. What are the income tax slabs for salaried individuals for AY 2024–25?

Income tax slabs are the same for salaried individuals as for other taxpayers. The slab system is not occupation-specific.

10. Is income up to ₹12 lakh tax-free for FY 2025–26?

- Yes, under the new tax regime.

- Income up to ₹4 lakh is taxed at nil rate.

- A rebate of ₹60,000 (u/s 87A) is available for income up to ₹12 lakh.

Thus, no tax is payable if your total income is ₹12 lakh or less.

11. How is senior citizen status determined for tax purposes

You are considered a:

- Senior citizen if you are 60 years or older on April 1, 2025.

- Super senior citizen if you are 80 years or older on the same date.

12. What are the income tax slabs for senior citizens under the old regime?

For individuals aged 60–79 years:

- Up to ₹3 lakh: Nil

- ₹3 lakh – ₹5 lakh: 5%

- ₹5 lakh – ₹10 lakh: 20%

- Above ₹10 lakh: 30%

Note: Under the new tax regime, slabs are uniform for all, regardless of age.

13. What are the tax slabs under the new regime for salaried individuals?

- Up to ₹3 lakh: Nil

- ₹3,00,001 – ₹7,00,000: 5%

- ₹7,00,001 – ₹10,00,000: 10%

- ₹10,00,001 – ₹12,00,000: 15%

- ₹12,00,001 – ₹15,00,000: 20%

- Above ₹15 lakh: 30%

- Standard deduction of ₹75,000 is available for salaried individuals.

15. Which tax regime is the default?

The new tax regime is the default for FY 2024–25. Taxpayers must actively opt out to use the old regime.

16. Which ITR form should I use based on my income slab?

ITR forms are not based on tax slabs but on sources and types of income. Refer to official guidelines or visit the Income Tax Department website to choose the correct ITR form.

17. How often do income tax slabs change?

Tax slabs are generally reviewed and may be changed annually during the Union Budget.

18. Are NRIs taxed under the same slabs as residents?

Yes, but NRIs:

- Do not receive higher exemption limits for senior/super senior citizens.

- Are not eligible for the rebate under Section 87A.