IndiaFilings

Expert

Published on: Jul 30, 2026

How To Form A Charitable Trust

A Trust is the obligation or responsibility placed on one in whom confidence or authority is place; it is a confidence reposed in a person by conveying to him the legal title to property which he is to hold for the benefit of others. Therefore, the "Trustee" responsibility includes protection of rightful ownership in the Trust property, the preservation of the Trust property and channelising the income from the Trust property in accordance with the intentions of the creator of the Trust. In this article, we look at the procedure for forming a Charitable Trust in India.

Definition of Charitable Trust in India

The The Indian Trusts Act, 1882 defines a Trust as an obligation annexed to the ownership of property, and arising out of a confidence reposed in and accepted by the owner, or declared and accepted by him, for the benefit of another, or of another and the owner.

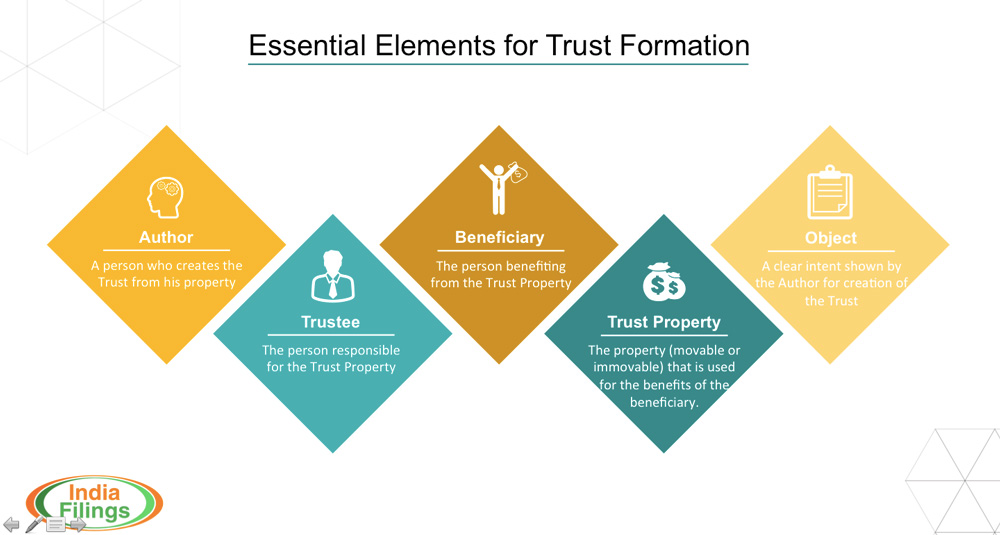

- The person who reposes or declares the confidence is called the "Author of the Trust".

- The person who accepts the confidence is called the "Trustee".

- The person for whose benefit the confidence is accepted is called the "Beneficiary".

- The subject-matter of the trust is called "Trust Property" or "Trust Money".

- The instrument if any, by which the Trust is declared is called the instrument of Trust or Trust Deed.

Essential Elements for Trust Formation

Essential Elements for Trust Formation

The following elements are essential for the formation of a Charitable Trust:

- An Author or Settlor of the Trust

- The Trustee

- The Beneficiary

- The Trust Property or the Subject Matter of the Trust

- The objects of the Trust

As per Section 6 of the The Indian Trusts Act, 1882 a Trust is created when the Author of the Trust indicates with reasonable certainty by any words or acts the following:

- An intention on his part to created a Trust

- The purpose of the Trust

- The Beneficiary

- The Trust Property

- And transfers the Trust Property to the Trustee.

Trust Deed

A Trust can be formed by words or act and there is no requirement for a Trust Deed. However, a Trust Deed is desirable and required in some cases. When a private Trust pertains to an immovable property a written and executed trust deed is essential and shall also required to be registered except where the Trust is created by a will. In case of public Trust for immovable property, a written Trust deed is not mandatory but desirable. In relation to Trusts for movable property (public or private), a simple delivery of possession with a direction that the property be held under Trust, is sufficient; it requires no document or registration.

Download a Sample Trust Deed Format

Reasons for forming a Charitable Trust

Charitable Trusts are formed in India for one or more of the following reasons:

- Discharge of the Charitable an/or religious sentiments of the Author, in a way that ensures public benefit.

- For claiming exemption from Income Tax, as the case may be, in respect of incomes applied to charitable or religious purposes.

- For the welfare of the members of the family and/or other relatives, who are dependent on the settlor of the Trust

- For the proper management and preservation of property.

- For regulating the affairs of a provident fund, superannuation fund or gratuity fund or any other fund constituted by a person for the welfare of its employees.

Procedure for forming a Charitable Trust

The procedure for forming a public Trust differs from that of private Trust, since they are governed by different laws. Creation of a public Trust is governed by the General law; whereas the creation of a private Trust is governed by the Indian Trusts Act. A public charitable or religious institution can be formed either as a Trust or as a Society or as a Section 8 Company. It generally takes the form of a Trust when its is instituted or formed primarily by one or few persons only. In this guide, we only cover the procedure for forming a private Charitable Trust.

Procedure for forming a Private Charitable Trust

For creating a private Trust, the foremost requirement is that the Author must express with reasonable certainty by words or acts, an intention on his part to create a Trust. Thus, a Trust may be declared either by words, spoken or written or by acts. Where a Trust is declared by words, the language used must be clear enough to show an intention to create a Trust. No formal language is required to constitute an effective declaration of Trust, but the language used must make it certain that:

- The Author intended to constitute a Trust binding in law on himself or the person to whom the property was given.

- The Author intended to bind definite property by the Trust.

- The Author intended to benefit a definite person or persons in a definite way.

For more information about Charitable Trust Formation, visit IndiaFilings.com