IndiaFilings

Expert

Published on: Apr 22, 2026

GST Ledgers

The GSTN maintains three different types of ledgers for tracking the payments, credits and liabilities of a person registered under GST.

Electronic Tax Liability Ledger

The electronic liability register maintains the liabilities of a taxpayer under GST. In the electronic liability register the tax due on filing a

GST return, interest, penalty and demands are maintained.Electronic Cash Ledger

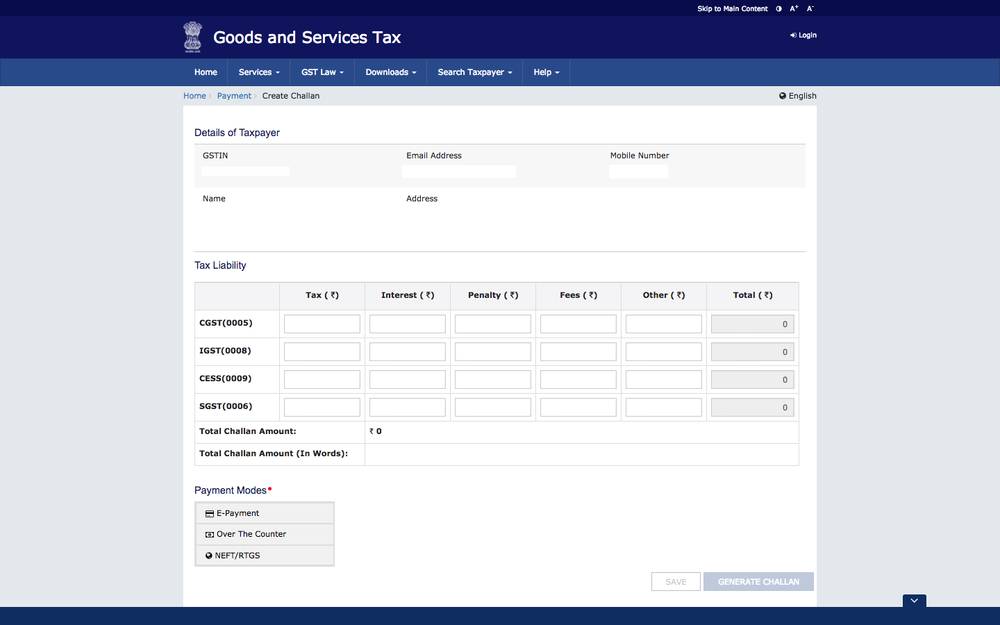

Whenever the taxpayer makes a GST payment through online banking, credit or debit card, wire transfer or over the counter payment, the amount paid shall reflect in the electronic cash ledger. For GST tax payment of above Rs.10,000, the taxpayer shall make the transactions only through official banking channels only. While making the GST payment, the taxpayer must provide the heads under regarding the payments, namely major heads of CGST, SGST, IGST and minor heads like tax, interest, penalty, fees and others. The electronic cash ledger shall display the balance based on the amount deposited through tax challan and heads. It shall also display the balance available under the various combination of the major-minor head.

GST Payment Challan

In addition to maintaining a record of GST payment made by the customer, the electronic cash ledger also contain credit for the amount deducted as TDS or TCS of the taxable person under GST.

Know more about electronic cash ledger.

GST Payment Challan

In addition to maintaining a record of GST payment made by the customer, the electronic cash ledger also contain credit for the amount deducted as TDS or TCS of the taxable person under GST.

Know more about electronic cash ledger.

Electronic Credit Ledger

The electronic credit ledger shall record all the taxes paid by the taxpayer on the inputs. The portal auto-populates the Electronic credit ledger based on the returns filed by the GST registered taxpayers on GSTR-1 and GSTR-2. The taxpayer can use the credit in the electronic credit ledger to offset GST liability in the following manner:

IGST Credit

After using the GST input tax credit for making payment of IGST, the taxpayer can use the remaining input tax credit to pay tax liability under CGST and at last SGST.

CGST Credit

The taxpayer can use the CGST input tax credit to pay IGST liability. However, CGST credit cannot be used to setoff the SGST liability.

SGST Credit

Using the SGST input tax credit, the taxpayer can use to pay for liability under IGST but cannot use SGST input tax credit to pay for the CGST liability. All the payments under GST have to be made by either using the input tax credit available in the electronic credit ledger or through the electronic cash ledger. A unique identification number shall be generated in the

GST common portal for each debit or credit to the electronic cash or credit ledger.Interest on Delayed Payment

All taxable persons must first pay the taxes and other dues (includes interest, penalty, fee or any other amount payable) of previous tax periods and thereafter for the current tax period. In case of delayed payment, interest will be levied at the rate of 18% per annum. In case of excess, ITC claimed / excess reduction in output tax liability by the taxpayer, interest will be charged at 24% per annum.

Know more about interest on delayed GST payment.