Bennisha

Expert

Published on: Jul 30, 2026

Gst Electronic Cash Ledger

The Electronic Cash Ledger is an account of the taxpayer that is maintained by the

GST system that reflects the cash deposits in recognized banks and payments of taxes and other dues made by the taxpayer. This contains a summary of all the deposits and payments that are made by a taxpayer. In the ledger, every information is kept minor head-wise for each major head. For the user’s convenience, the ledger is displayed major head-wise such as IGST, CGST, SGST/UTGST, and CESS. Every minor head is classified into five minor heads, which are Tax, Interest, Penalty, Fee, and Others. In this article, we look at the procedure for viewing the electronic cash ledger on the GST Portal.Electronic Cash Ledger

The electronic cash ledger should be maintained in Form-GST PMP-05 on the common portal for the person liable to pay tax, interest, late fee, penalty or any other amount. The registered taxpayer should generate a challan in Form GST PMT-06 on the common portal and then enter the details of the amount deposited towards tax, penalty, fees, interest or any other amount.Methods for Deposit

The deposit can be made using any of the following methods:- Internet banking through authorised banks

- Debit or credit card through authorised banks

- National Electronic Fund Transfer (NEFT)

- Real-Time Gross Settlement (RTGS)

- Counter payment through authorised banks for a deposit up to Rs.10,000 per challan can be made by cheque, cash or demand draft. However, the restriction for deposit does not apply to the deposit made by any of the following entities:

- Government department or any deposit specified by the commissioner

- Proper officer authorised to recover outstanding due from the unregistered or registered person.

- Proper officer authorised to collect to amount in the form of cash, cheque or demand draft during any investigation.

Payment through NEFT or RTGS

- In addition to the above, the registered taxpayer can make payment through National Electronic Fund Transfer or Real Time Gross Settlement from the bank. Then the mandate form along with the challan generated on the common portal needs to be submitted to the bank. The validity period of this mandate form is 15 days from the date of the challan generated.

- On making payment successfully, the collecting bank generates a Challan Identification Number (CIN) and the same will be indicated in the challan.

- On receipt of the Challan Identification Number (CIN) from the collecting bank, the amount will be credited to the ledger of the registered taxable person.

- In cases when bank debits your account on making deposit but fails to generate Challan Identification number or the CIN which is generated by the bank not uploaded in the common portal. In such cases, the concerned person can submit an application electronically through Form GST PMT-07.

Credit of Electronic Cash Ledger

Any amount deducted or collected under GST can be claimed by the registered taxpayer and the same will be credited to the electronic cash ledger of the registered taxpayer.Debit of Electronic Cash Ledger

The amount from the electronic cash ledger is debited if a registered taxpayer has claimed for any refund from the ledger itself.Rejection of Refund

In case of the amount claimed is rejected either fully or partly, the amount debited so far will be credited to the cash ledger by the proper officer using a Form GST PMT-03.Viewing Electronic Cash Ledger

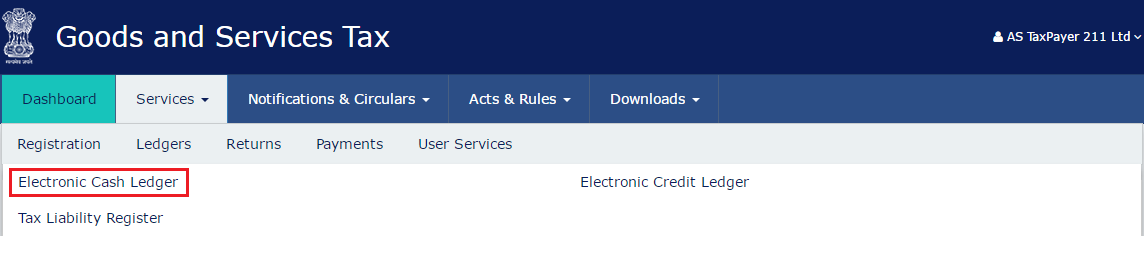

Electronic Cash Ledger can be viewed by the taxpayers themselves, or through their authorized signatories and

GST Practitioner. Moreover, this can be viewed by their Jurisdictional Officials (JO). Here are the steps to view an Electronic Cash Ledger. Step 1: Login to the Portal The taxpayer has to login to the official GST Portal. Step 2: Enter the Credentials The taxpayer has to enter the username and password. Step 3: Click Electronic Cash Ledger From the ‘Services’ tab, the taxpayer has to click on the ‘Ledgers’ option and then click on ‘Electronic Cash Ledger’ command. The Electronic Cash Ledger page is displayed on the screen. Step 3-Gst Electronic Cash Ledger

Step 4: Cash Balance

Under the ‘Cash Balance as on Date’ column, the cash balance is displayed. The taxpayer can also click the link for the amount displayed under Cash Balance as on Date to get a summary of the cash balance

Step 5: Click Electronic Cash Ledger

The taxpayer has to click the ‘Electronic Cash Ledger’.

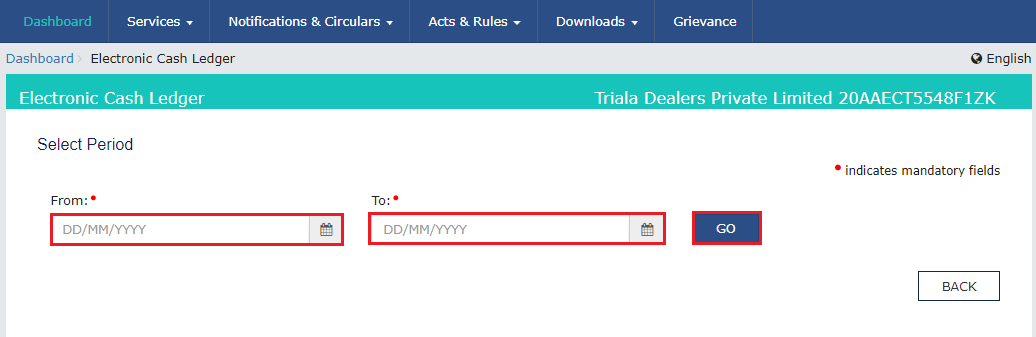

Step 6: Select the time period

The taxpayer using the calendar has to select the ‘From’ and ‘To’ time period for which the Electronic Cash Ledger has to be viewed.

Step 7: Click GO

The taxpayer has to click the ‘Go’ button. The Electronic Cash Ledger can be viewed only for a maximum period of six months. The Electronic Cash Ledger details are displayed on the screen.

Step 3-Gst Electronic Cash Ledger

Step 4: Cash Balance

Under the ‘Cash Balance as on Date’ column, the cash balance is displayed. The taxpayer can also click the link for the amount displayed under Cash Balance as on Date to get a summary of the cash balance

Step 5: Click Electronic Cash Ledger

The taxpayer has to click the ‘Electronic Cash Ledger’.

Step 6: Select the time period

The taxpayer using the calendar has to select the ‘From’ and ‘To’ time period for which the Electronic Cash Ledger has to be viewed.

Step 7: Click GO

The taxpayer has to click the ‘Go’ button. The Electronic Cash Ledger can be viewed only for a maximum period of six months. The Electronic Cash Ledger details are displayed on the screen.

Step 7-Gst Electronic Cash Ledger

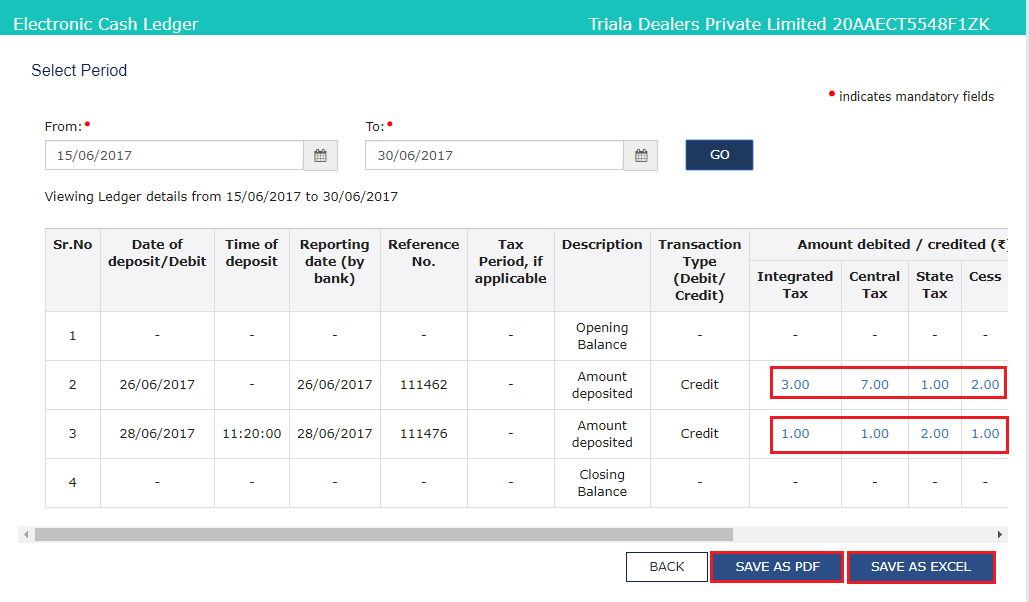

Step 8: Click Save

The taxpayer has to either click on ‘Save as PDF’ or ‘Save as Excel’ button to save the Electronic Cash Ledger.

Step 7-Gst Electronic Cash Ledger

Step 8: Click Save

The taxpayer has to either click on ‘Save as PDF’ or ‘Save as Excel’ button to save the Electronic Cash Ledger.

- By clicking the ‘Save as PDF’ button, the Electronic Cash Ledger is saved in the PDF format.

- By clicking the ‘Save as Excel’ button, the Electronic Cash Ledger is saved in the excel format.

Step 8-Gst Electronic Cash Ledger

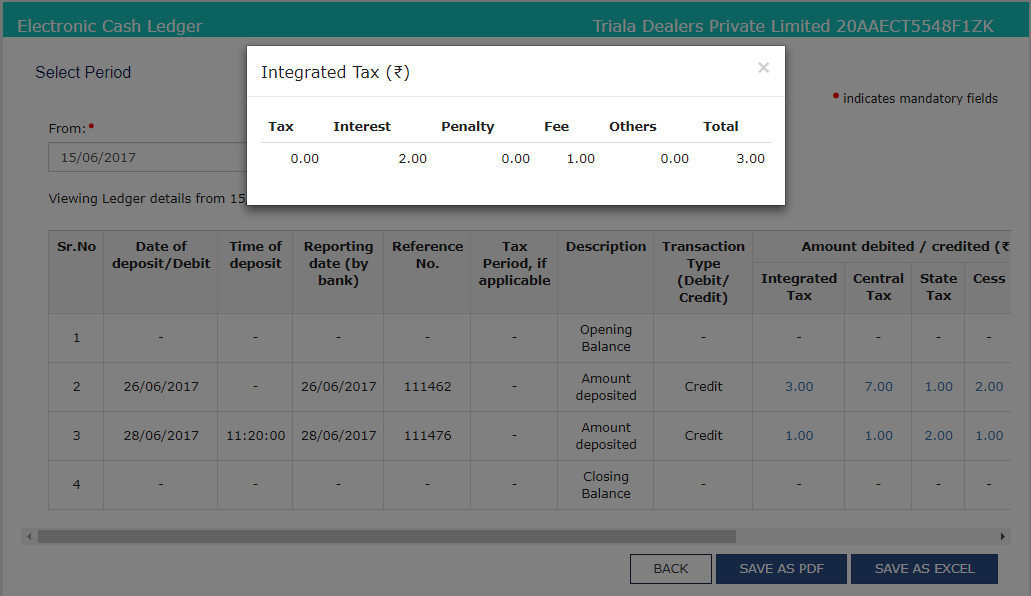

The taxpayer can click the amount displayed under any of the Major Heads to view the Minor Heads details. The pop-up window appears with the concerned Minor Head details of the selected Major Head.

Step 8-Gst Electronic Cash Ledger

The taxpayer can click the amount displayed under any of the Major Heads to view the Minor Heads details. The pop-up window appears with the concerned Minor Head details of the selected Major Head.

Step 8-Gst Electronic Cash Ledger

Step 8-Gst Electronic Cash Ledger

Viewing Details of Transactions

The taxpayer can view the details of the transactions that are made in the Electronic Cash Ledger for a specific duration. This option is available on the landing page of the Electronic Cash Ledger. A maximum of six months transactions can be viewed at a time.

Deposit Update in the Cash Ledger

Once the payment is done, the deposit update in the cash ledger will be made as given below.

| Mode of Payment | Deposit update in the Cash Ledger |

| Online payment by net banking in authorized Banks | On receipt of CIN from the bank. It is usually shared by the bank instantly but at times there may be a delay. |

| OTC payment made by cash and self-bank cheque in authorized banks | On receipt of CIN from the bank. It is usually shared by the bank instantly on receipt of cash or realization of cheque but sometimes there may be a delay |

| OTC payment made through other bank cheques of the same station in authorized Banks | On receipt of CIN from the bank. In the case of cheques Banks are given 90 days’ time period to share the CIN details |

| OTC payment made through other outstation bank cheques in authorized Banks | On receipt of CIN from the bank. In the case of cheques Banks are given 90 days’ time period to share the CIN details |

| Online NEFT/RTGS payments made through non-authorized but recognized Banks | As soon as RBI shares CIN details. Usually can be on the same day. |

| Over the counter NEFT/RTGS payments made through non-authorized Banks | As soon as RBI shares CIN details. Usually can be on the same day. |

| Payment through Credit Card/Debit Card | After 24 hours of Payment. But once the amount is debited and Payment Gateway confirms the receipt of the amount, Banks are given 45 days time to confirm the payment and then the cash ledger will be updated after final confirmation from the bank. |

After the payment, CIN is reported by the Bank to the GST system along with a unique reference number that is generated by the banking system that gets captured in the electronic cash ledger of the taxpayer. The Electronic Cash Ledger is updated within some time. For outstation cheque that is in OTC mode, CIN and the Bank Reference Number (BRN) is reported by the bank to the GST system when the cheque is realized and the amount is then credited to the government account from the taxpayer’s account. On receipt to the CIN, the Cash Ledger is updated within some time.

Filing of GST PMT-04

If the payments made through the challan are not reflected in the cash ledger, the taxpayer has to raise a grievance on the GST Portal using GST PMT-04 form. Know more about

GST payment issues.Checking Balance

The taxpayer can check the available balance in the Electronic Cash Ledger by selecting the ‘Services’ tab, the ‘Ledgers’ option and then click on ‘Electronic Cash Ledger’. The balance is shown on the right-hand corner under the head ‘Cash Balance as on Date’. A brief summary of the major head wise balance is given when the cursor is placed on the same. To know additional details of the transaction, the taxpayer has to submit a request for the report by giving the date range. The total amount available in the Electronic Cash Ledger can be used for the payment of any liability for the concerned major and minor heads.