Renu Suresh

Expert

Published on: Jul 30, 2026

e-Invoicing under GST: Applicability, Rules, Process & Effective Dates of Implementation

e-Invoicing under GST refers to the mandatory system of electronic invoicing introduced by the Goods and Services Tax (GST) regime to standardise and digitise Business-to-Business (B2B) transactions. Just as GST-registered businesses must generate an e-way bill for transporting goods, those with an annual turnover exceeding ₹10 crores are required to issue invoices in a standardised electronic format through the government-designated portal. This move aims to streamline invoicing processes, enhance GST compliance, reduce manual errors, and curb tax evasion. With e-invoicing becoming a critical compliance requirement, it is essential for businesses to understand its applicability, generation process, mandatory fields, and the effective dates of implementation to avoid penalties and ensure smooth operations.

IndiaFilings’ LEDGERS GST invoicing software simplifies e-invoice generation by automating the entire process after a one-time activation. Whether through web, mobile, Excel, or API, businesses can effortlessly create and share GST-compliant e-Invoices with QR codes in real-time.

Key Ideas & Updates on GST e-invoicing

- Revised Turnover Threshold - ₹5 Crore+ from August 2023: E-invoicing became mandatory for businesses with an Annual Aggregate Turnover (AATO) exceeding ₹5 crore, effective August 2023, reducing the earlier limit.

- Previous Threshold - ₹10 Crore+ Businesses Only: Before the update, only businesses with a turnover above ₹10 crore were required to comply with e-invoicing provisions.

- 30-Day Invoice Upload Rule from April 2025: From 1st April 2025, businesses with ₹10 crore+ turnover must upload e-invoices to the Invoice Registration Portal (IRP) within 30 days of invoice generation.

- Case-Insensitive Invoice Numbers from June 2025: Effective 1st June 2025, IRP will treat invoice numbers as case-insensitive, automatically converting all to uppercase before Invoice Reference Number (IRN) generation. This change aligns with GSTR-1 invoice data handling.

- Mandatory 2FA Authentication for All Taxpayers by April 2025: As per the 17th December 2024 advisory, two-factor authentication (2FA) becomes mandatory for:

- Businesses with ₹20 crore+ turnover from 1st Jan 2025

- Businesses with ₹5–20 crore turnover from 1st Feb 2025

- All taxpayers, regardless of turnover, from 1st April 2025

- e-Way Bill Generation Limit -180 Days from Invoice Date: Starting 1st Jan 2025, taxpayers must generate e-way bills within 180 days of the invoice or document date.

- e-Way Bill Validity Extension - Max 360 Days: From 1st Jan 2025, e-way bill validity extensions are limited to 360 days from the original generation date.

- 30-Day e-Invoice Rule Enforcement Date Confirmed: The 30-day time limit for reporting e-invoices on IRP portals for ₹10 crore+ turnover businesses will take effect from 1st April 2025, as announced on 5th November 2024.

- B2C e-Invoicing May Come Soon: On 9th September 2024, the GST Council recommended a phased rollout of e-invoicing for B2C transactions, expanding its scope beyond B2B invoicing for registered persons.

What is e-Invoicing under GST?

E-invoicing, or electronic invoicing, is a system introduced under the Goods and Services Tax (GST) regime for the digital authentication of B2B invoices and select other documents. Initially recommended in the 35th GST Council Meeting, it was first applicable to large enterprises and gradually expanded to mid-sized and small businesses. Under this system, businesses do not generate invoices directly on the GST portal; instead, they prepare invoices in a standard format and upload them to a designated Invoice Registration Portal (IRP) notified by the Central Board of Indirect Taxes and Customs (CBIC) through Notification No. 69/2019 – Central Tax.

The first such IRP was launched by the National Informatics Centre, managed by the GST Network (GSTN). Once uploaded, each invoice is electronically authenticated and assigned a unique Invoice Reference Number (IRN), automating the exchange of data between the GST portal, e-way bill portal, and the taxpayer.

E-invoicing significantly reduces manual data entry errors and streamlines compliance. All invoice details submitted to the IRP are shared in real-time with the GST portal and the e-way bill system, facilitating automatic population of GSTR-1 returns and generation of Part-A of e-way bills. E-invoices must comply with a standardised format prescribed by GST authorities and include key elements like the IRN and a QR code, which encodes vital invoice information for easy verification by tax officers.

Benefits of e-Invoicing Under GST

The implementation of e-invoicing under GST offers numerous benefits for both businesses and tax authorities, promoting greater transparency, automation, and compliance across the tax ecosystem:

- Minimises Data Mismatch Errors: E-invoicing helps resolve data reconciliation issues under GST by ensuring uniform reporting, significantly reducing mismatch errors during return filing.

- Supports Interoperability Across Systems: E-invoices generated from one accounting software can be seamlessly read by another, promoting system interoperability and minimising manual data entry errors.

- Enables Real-Time Invoice Tracking: Businesses can track invoices prepared by suppliers in real-time through the Invoice Registration Portal (IRP), enhancing supply chain visibility.

- Automates GST Return Filing: E-invoicing supports backwards integration, allowing auto-population of invoice details into GST returns and e-way bills, especially Part-A of e-way bills.

- Speeds Up Input Tax Credit (ITC) Claims: With authenticated invoice data readily available to the GST system, businesses can claim genuine input tax credit faster and more accurately.

- Reduces Need for Tax Audits and Surveys: Since transaction-level data is readily available to tax authorities, the need for frequent audits or field surveys reduces significantly.

- Improves Access to Credit for Small Businesses: E-invoices enable faster processing of invoice financing and discounting, making formal credit more accessible, especially to MSMEs.

- Builds Trust with Large Enterprises: Compliance with e-invoicing requirements improves business credibility and enhances the chances of collaborating with larger companies.

- Limits Invoice Manipulation and Fraud: As e-invoices must be pre-verified through the GST portal, it reduces the scope for invoice tampering and issuance of fake invoices.

- Prevents Fake ITC Claims: Since all invoices are registered with GSTN, the system can easily detect discrepancies, ensuring that only genuine input tax credit is claimed.

- Enhances Transparency for Tax Authorities: E-invoicing provides tax officials with real-time access to invoice data, allowing effective monitoring of transactions and tax compliance.

Applicability of e-Invoicing under GST: Who must generate e-Invoices?

E-invoicing under GST is mandatory for businesses whose aggregate turnover exceeds specified limits, as notified by the government in various phases. Importantly, the threshold is checked for any financial year from 2017-18 onwards, not just the current year.

Note: If a business crosses the threshold in the current year, e-invoicing becomes applicable from the beginning of the next financial year.

Table: Turnover Criteria and Applicability of GST Invoice

Phase | Aggregate Turnover Exceeds | Effective date of implementation | Notification Number | Relevant Financial Years for Turnover Calculation |

I | Rs 500 crore | 01.10.2020 | FY 2017-18 onwards | |

II | Rs 100 crore | 01.01.2021 | ||

III | Rs 50 crore | 01.04.2021 | ||

IV | Rs 20 crore | 01.04.2022 | ||

V | Rs 10 crore | 01.10.2022 | ||

VI | Rs 5 crore | 01.08.2023 |

How Applicability Works: Examples (in this perspective)

Example 1: XYZ Traders

- Turnover History:

- FY 2017-18: Rs 3 crore

- FY 2018-19: Rs 4 crore

- FY 2019-20: Rs 7 crore

- FY 2020-21: Rs 6 crore

- FY 2021-22: Rs 5.5 crore

- FY 2022-23: Rs 5.2 crore

- FY 2023-24: Rs 6.1 crore

- Analysis: XYZ Traders crossed the Rs 5 crore threshold for the first time in FY 2023-24.Applicability: They must start generating e-invoices from the beginning of the next financial year, i.e., from 1st April 2025.

Example 2: LMN Enterprises

- Turnover History:

- FY 2017-18: Rs 12 crore

- FY 2018-19: Rs 15 crore

- FY 2019-20: Rs 18 crore

- FY 2020-21: Rs 22 crore

- FY 2021-22: Rs 19 crore

- Analysis: LMN Enterprises crossed the Rs 20 crore threshold in FY 2020-21.Applicability: They are required to generate e-invoices from 1st April 2022, as per the phase IV notification, regardless of whether their turnover fell below the threshold in subsequent years.

Which Transactions and Documents does e-Invoicing apply to?

The e-invoicing system under GST applies to specific types of transactions and documents as mandated by law. Below is a breakdown of applicable documents and transactions:

- Applicable Documents: E-invoicing is mandatory for the following document types issued under Section 34 of the CGST Act:

- Tax Invoices

- Credit Notes

- Debit Notes

- Applicable Transactions: The following types of transactions are covered under e-invoicing requirements:

- Business-to-Business (B2B) supply of goods or services

- Business-to-Government (B2G) transactions involving supply of goods or services to government entities

- Export of goods or services, including zero-rated supplies

- Deemed Exports as notified under GST law

- Supplies to Special Economic Zones (SEZ) – with or without payment of tax

- Stock transfers or supply to distinct persons as per Section 25(4) of the CGST Act

- Supplies to SEZ Developers

- Reverse Charge Mechanism (RCM) supplies covered under Section 9(3) of the CGST Act

These transactions must be reported through the Invoice Registration Portal (IRP) to generate a valid e-invoice.

Who does not need to comply with GST e-invoicing?

The following categories of registered persons are exempt from the e-invoicing requirements under GST:

- Banks, Insurers & Financial Institutions: Suppliers of taxable services who are insurers, banks, financial institutions, or non-banking financial companies (NBFCs) are not required to generate e-invoices.

- Goods Transport Agencies (GTAs): When the service provider is a goods transport agency offering transportation of goods by road in a goods carriage, e-invoicing is not applicable.

- Passenger Transport Service Providers: Businesses engaged in providing passenger transportation services are exempt from e-invoicing provisions.

- Multiplex Cinema Exhibitors: Registered persons offering admission to cinematograph film exhibitions on multiplex screens are not subject to e-invoicing compliance.

- SEZ Units: Units operating within Special Economic Zones (SEZs) are exempt from e-invoicing, although this exemption does not extend to SEZ developers.

- Government Departments and Local Authorities: Government bodies and local authorities are not required to follow e-invoicing norms under GST.

- Persons Registered Under Rule 14 of CGST Rules: Those registered under Rule 14 of the CGST Rules are also excluded from the scope of e-invoicing.

What is the Time Limit to Generate E-invoices?

The time limit to generate e-invoices under GST is not fixed while this mandate is issued. It evolved over the period of time. Here is the comprehensive timeline chart detailing the date and the relevant updates regarding the e-Invoice time limit:

Date | Time Limit Updates |

Until 30th April 2023 | No specific time limit was prescribed under GST law for generating e-invoices. Businesses could generate and report invoices without a fixed deadline. |

1st May 2023 (Announced) | Government proposed a 7-day time limit for e-invoice generation for businesses with AATO ≥ ₹100 crore, but this rule was not implemented. |

1st November 2023 | A 30-day time limit was officially mandated for businesses with AATO ≥ ₹100 crore to report tax invoices, credit notes, and debit notes to an IRP. |

5th November 2024 (Advisory) | The 30-day reporting rule was extended to businesses with AATO ≥ ₹10 crore, with the change to be implemented from 1st April 2025. |

1st April 2025 (Effective Date) | The 30-day e-invoice reporting requirement becomes applicable to all taxpayers with AATO of ₹10 crore or more. |

Let’s understand the format, contents and the process to generate and get e-invoices under GST.

What are the Mandatory Fields in the e-Invoice under GST?

E-invoice must adhere to the GST invoicing rules prescribed by the government. It must follow the rules prescribed by the specific industries or sectors. Several fields are mandatory in the e-invoice, where the relevant information must be included by the taxpayers. Let’s understand the overall contents and mandatory fields of the GST invoice.

Gist of Contents in GST e-Invoicing

The GST e-invoice format, as notified on 30th July 2020 (Notification No. 60/2020 – Central Tax), is structured to standardize and streamline invoicing across businesses. The format comprises 12 sections (both mandatory and optional) and six annexures, totaling 138 fields. Out of these, five sections and two annexures are mandatory:

Mandatory Sections:

- Basic details

- Supplier information

- Recipient information

- Invoice item details

- Document total

Mandatory Annexures:

- Details of the items

- Document total

Table: Mandatory Fields of GST e-Invoice

Section | Field Name | Description |

Document Details | Document Type Code | Type of document (Invoice, Credit Note, Debit Note, etc.) |

Document Number | Unique invoice number for the financial year | |

Document Date | Date of invoice in DD/MM/YYYY format | |

Supplier Details | Supplier Legal Name | Name as per PAN |

Supplier GSTIN | GST Identification Number of supplier | |

Supplier Address | Full address, including place, pin code, state code | |

Recipient Details | Recipient Legal Name | Name as per PAN |

Recipient GSTIN | GST Identification Number of recipient | |

Recipient Address | Full address, including place, pin code, state code | |

Place of Supply | State code where supply is made | |

Invoice Item Details | Item Description | Description of goods/services |

HSN Code | Harmonized System of Nomenclature code | |

Quantity | Quantity of goods/services | |

Unit | Unit of measurement (e.g., Nos, Kg) | |

Item Price | Unit price excluding GST | |

Assessable Value | Value after discount, excluding GST | |

GST Rate | Applicable GST rate (%) | |

IGST Value | Integrated GST amount | |

CGST Value | Central GST amount | |

SGST Value | State GST amount | |

Document Total | Total Invoice Value | Total value including GST |

Total Taxable Value | Total taxable value (excluding GST) | |

Additional Details | IRN (Invoice Reference Number) | Unique number generated by IRP |

QR Code | QR code generated by IRP | |

Shipping To GSTIN | GSTIN of recipient for shipping | |

Shipping To State, Pincode | State and pin code for shipping | |

Dispatch From Name, Address | Name and address of dispatching entity | |

Supply Type Code | Code indicating type of supply (B2B, SEZ, etc.) | |

Is Service | Whether supply is a service |

Sample e-Invoice Format

Below, we have attached the sample GST e-invoice to help you understand the format and structure of the contents.

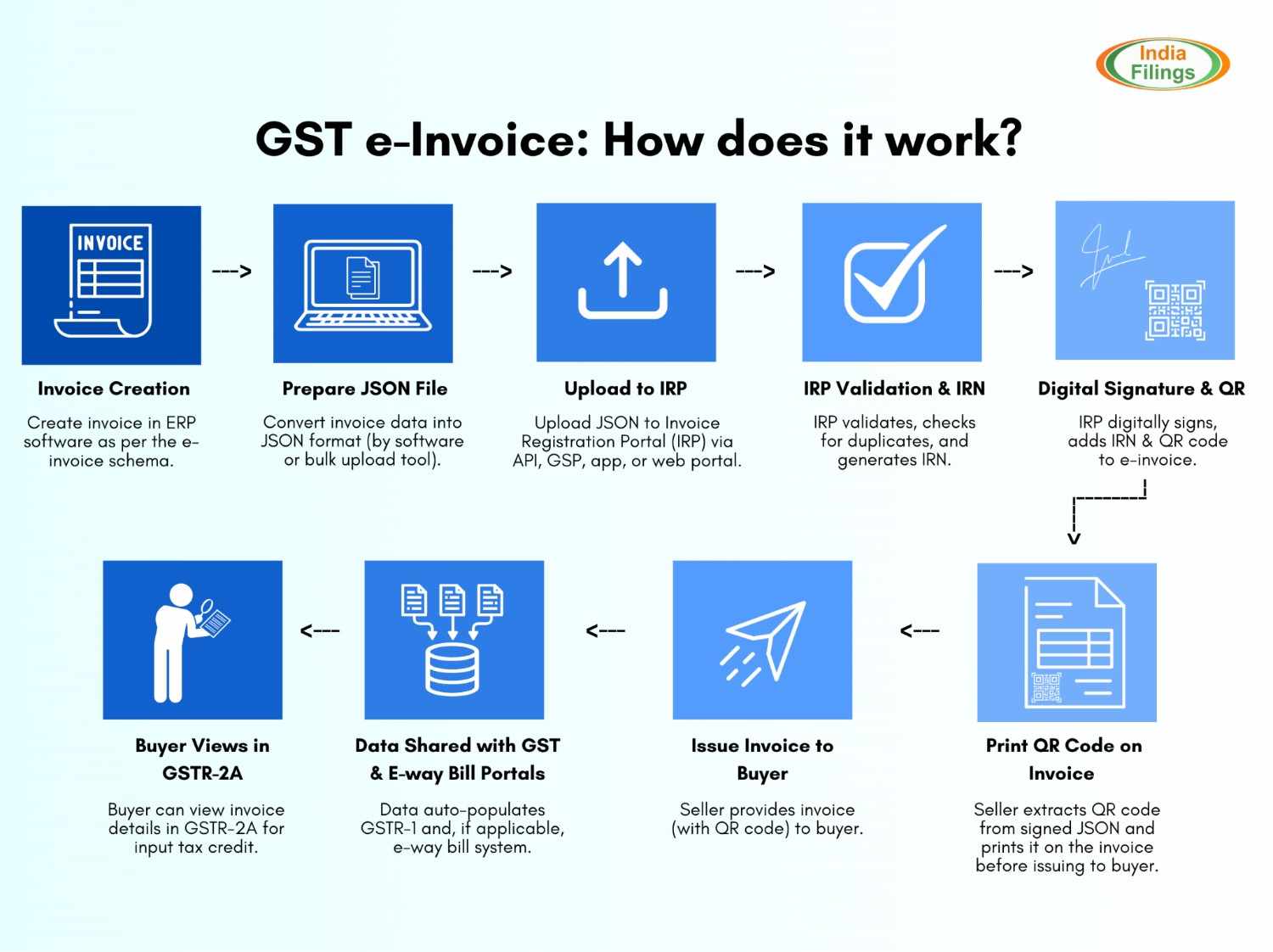

What is the process to generate & get an e-Invoice?

There are multiple stages involved in generating and getting an invoice. We’ll discuss the process in this section,

1. Configure Your ERP/Billing System

First, the taxpayer must ensure their ERP or billing software is updated to align with the PEPPOL standards and the e-invoice schema notified by the CBIC. This may require coordination with your software provider to incorporate all mandatory fields and technical specifications required for e-invoicing.

2. Choose an Integration Method

There are two primary ways to connect with the Invoice Registration Portal (IRP):

- Direct API Integration: The taxpayer’s system IP address can be whitelisted for direct API access, or integration can be established via a GST Suvidha Provider (GSP).

- Bulk Upload Tool: Alternatively, taxpayers can use the bulk generation tool to prepare invoice data in a JSON format, which is then uploaded in bulk to the IRP.

3. Generate the Invoice

Create the invoice using your ERP or billing software, ensuring all mandatory details—such as supplier and recipient information, GSTINs, invoice value, item details, and tax rates—are included and accurate.

4. Upload Invoice Data to IRP

Upload the invoice details to the IRP. This can be done:

- By uploading the JSON file generated from your software,

- Through an integrated application (app), or

- Via a GSP or direct API connection.

- The IRP also supports other submission modes, such as SMS-based or mobile app-based uploads, for added flexibility.

5. Validation and IRN Generation

The IRP validates the uploaded invoice data, checks for duplicates, and generates a unique Invoice Reference Number (IRN) using key parameters: Seller GSTIN, invoice number, financial year, and document type. The IRP then digitally signs the invoice and creates a QR code in the output JSON.

6. Receive Authenticated Invoice

Once validated, the IRP returns the authenticated e-invoice, complete with the IRN and QR code, to the taxpayer. If an email address is provided in the invoice, the seller is notified via email as well.

7. Auto-Population in GST Returns and E-way Bill

The IRP forwards the authenticated invoice data to the GST portal for auto-population in GSTR-1 and, if applicable, to the e-way bill portal. This ensures that your tax returns and e-way bill requirements are automatically updated, streamlining compliance and reducing manual effort.

How LEDGERS GST E-invoicing Software Helps?

Simplify your GST compliance with IndiaFilings’ LEDGERS GST e-Invoicing Software—a powerful solution designed to automate and streamline e-invoice generation for your business. Once activated, LEDGERS seamlessly integrates with the government’s GST e-Invoicing system to auto-generate e-Invoices for all B2B transactions.

With LEDGERS, you can:

- Instantly generate e-Invoices from your web browser, Android, or iOS device

- Use Excel uploads or API integration for bulk invoicing

- Automatically issue e-Invoices post activation—no manual uploads required

- Share invoices with QR codes instantly via email, SMS, or WhatsApp

Start generating GST-compliant e-Invoices within minutes and ensure error-free, real-time compliance with LEDGERS—your trusted partner for smart GST invoicing.

FAQs

1. What is a GST e-invoice?

A GST e-invoice is a digitally reported B2B or export invoice that has been validated by the IRP, assigned a unique IRN, and contains a QR code as proof of authenticity under GST law.

2. What is e-invoice software?

E-invoice software is a digital tool or platform that helps businesses generate, manage, and report GST-compliant e-invoices in the required format. It often integrates with accounting systems and connects directly to the Invoice Registration Portal (IRP) for seamless IRN generation and compliance.

3. How do I log in to the e-invoice portal?

You can log in to the e-invoice portal using your GSTIN and registered credentials. New users must first register on the portal before accessing e-invoicing services.

4. What is the e-invoice portal?

The e-invoice portal (such as einvoice1.gst.gov.in) is the official government platform where taxpayers upload invoice data for validation, IRN generation, and QR code assignment under the GST e-invoicing system.

5. What is the current e-invoice limit under GST?

As of August 2023, e-invoicing is mandatory for businesses with an aggregate turnover exceeding Rs. 5 crore in any financial year from 2017-18 onwards.

6. Who is required to generate e-invoices under GST?

E-invoicing applies to GST-registered businesses whose aggregate turnover exceeds the notified threshold (currently Rs. 5 crore), except for certain exempted categories like SEZ units, banks, and transport agencies.

7. How does the e-invoice system work?

Businesses generate invoices in their accounting software, upload them to the IRP for validation, receive a unique IRN and QR code, and then issue the authenticated invoice to the buyer. The data is auto-shared with the GST and e-way bill portals.

8. How is turnover calculated for e-invoice applicability?

The aggregate turnover is calculated PAN-wise across all GSTINs in India, considering all financial years from 2017-18 onwards. If turnover exceeds Rs. 5 crore in any year, e-invoicing is mandatory.

9. What are common technical issues faced with e-invoice portals?

Technical issues include slow response times, system downtime during peak periods, integration difficulties with business applications, and occasional server outages. These can disrupt business operations and are often due to high portal traffic or technical glitches.

10. What are the most frequent errors encountered during e-invoice generation?

Common errors include duplicate invoice reference numbers, invalid or incorrect invoice data, incorrect HSN codes, mismatched taxable values, and missing mandatory fields. Each error has a specific code and resolution, such as correcting data or ensuring unique invoice numbers.

11. How can I resolve a duplicate IRN error?

A duplicate IRN error occurs when the same invoice is uploaded more than once. To resolve this, avoid resubmitting the same invoice request and ensure your system updates with the IRN received from the IRP before any further submissions.

12. Is e-invoicing applicable to SEZ units or unregistered persons?

No, e-invoicing is not applicable to SEZ units and cannot be generated for unregistered persons (URP) in B2B transactions.

13. What should I do if the e-invoice portal is not working?

If the portal is down, it may be due to server overload, scheduled maintenance, or connectivity issues. Wait for the portal to become available, check official notifications, or try accessing it during off-peak hours.

14. What are some common mistakes to avoid in e-invoicing?

- Not keeping up with the latest e-invoicing updates

- Sending B2C invoice data to the IRP (only B2B and exports are allowed)

- Failing to validate all mandatory fields and formats before submission

15. What happens if mandatory fields are missing in the e-invoice?

The IRP will reject the invoice, and you must correct the missing or invalid data before resubmitting. Missing fields can also lead to compliance issues and delays in GST return filing.

16. How does e-invoicing help in GST reconciliation?

E-invoicing standardizes invoice data and auto-populates GSTR-1, reducing manual errors and mismatches during GST reconciliation, thus simplifying compliance.

17. Can I generate e-invoices in bulk?

Yes, you can use the bulk upload tool to generate multiple e-invoices at once by preparing and uploading a JSON file to the IRP.

18. Is it mandatory to print the QR code on the e-invoice?

Yes, the QR code generated by the IRP must be printed on the invoice issued to the buyer. This is essential for validation and compliance.