Sreeram Viswanath

Expert

Published on: Mar 28, 2026

Form INV-01

Form INV-01 holds a place of significance in the Indian GST regime, thanks to the provision of Invoice Reference Number (IRN). Invoice Reference Number (IRN) is an alternative to the conventional system of invoicing wherein an original invoice is maintained by the buyer, a duplicate is issued to the transporter, and triplicate to the seller. The option digitizes the revenue process at the check posts, reduces the waiting time for the transporter at revenue check posts and enables tax authorities to track the goods being transported without referring to the duplicate copy. As the nature of the invoice isn’t physical, it takes away the risk of loss. IRN could be generated from the eway bill portal by uploading an invoice (Form GST INV-01). The number so generated would be valid for a period of 30 days, within which it can be used in place of a physical tax invoice. This article particularly centres around Form GST INV-01 and its particulars.

Format Explained

As already observed, GST INV-01 must be uploaded into the portal so as to generate the IRN. The form comprises of four parts with different particulars to be filed in each of them. Such particulars are covered here for the awareness of the readers:

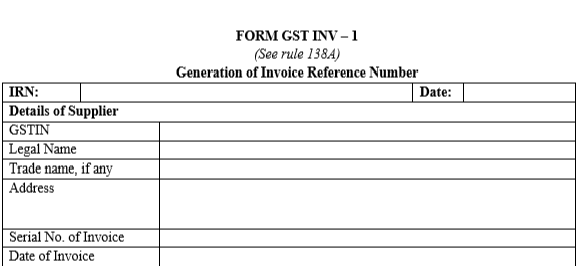

Part A

The form begins by asking taxpayers/suppliers to fill in their basic details, which includes:

- GSTIN and the name of the supplier (auto-populated).

- The address of the registered/principal place of business.

- Serial number and the date of invoice.

Form GST INV 1 - Part A

Form GST INV 1 - Part A

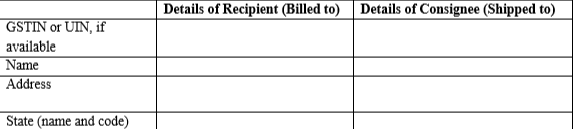

Part B

This part of the form pertains to the details of the recipient, which includes:

- GSTIN (for registered taxpayers).

- UIN (if the recipient is an embassy or UN organization).

- The name of the recipient and consignee.

- The address and state code (first two digits of the GSTIN) of the consignee.

For the awareness of the taxpayers, the details of the consignee and recipient could be similar if the parties being billed to and the parties to whom the goods are being delivered are identical. In certain cases, though, the GSTIN of both the recipient and consignee can be the same but with different addresses. And in other instances, the GSTIN of the party to whom the bill is addressed to would differ from the one to whom it is shipped.

Form GST INV Part B

Form GST INV Part B

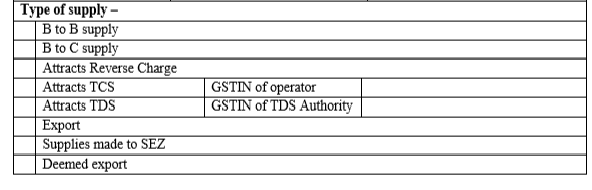

Part C

Part C of the Form deals with particulars concerning the type of supply made by the taxpayer, including the type of transaction and applicability for tax provisions.

Form GST INV 1 - Part 3

Form GST INV 1 - Part 3

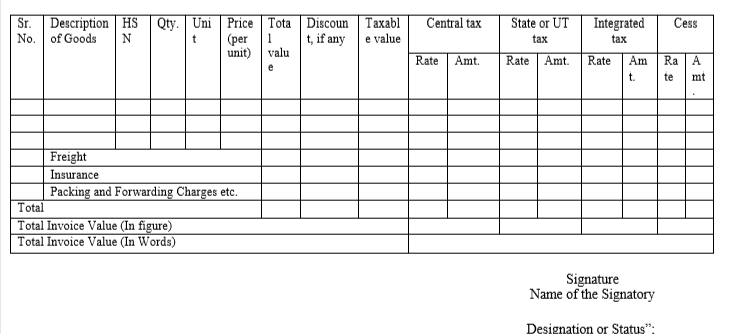

Part D

The final part of the form prompts for information pertaining to the consignment of goods billed, which includes:

- The description of goods.

- The HSN code.

- The quantity and unit price, which helps in determining the taxable GST amount.

- The applicable tax rate and amount, which will be calculated based on the type of transaction (inter-state or intra-state).

- The declaration of freight, invoice and packaging and forwarding charges as stated in the tax invoice.

Form GST INV 1 - Part D

HSN Code – Harmonized System Nomenclature Code is an internationally recognized classification method. It has been employed by the Indian Government to classify goods under GST and levy of taxes under the tax system.

Form GST INV 1 - Part D

HSN Code – Harmonized System Nomenclature Code is an internationally recognized classification method. It has been employed by the Indian Government to classify goods under GST and levy of taxes under the tax system.