IndiaFilings

Expert

Published on: Apr 22, 2026

Form 10IA - Section 80DD Deduction

Form 10IA of the Income Tax Department must be filed by taxpayers claiming

income tax deduction under Section 80DD. Section 80DD deduction can be claimed by taxpayer, both individuals and HUF, supporting a disabled dependent. The maximum deduction allowed under section 80DD is Rs.75,000 for dependents with disability. For maximum deduction allowed under Section 80DD is increased to Rs.1,25,000 for taxpayers supporting a disabled dependent with severe disability.What is Section 80DD?

Section 80DD deduction can be claimed by individuals who are resident in India and HUFs for maintenance and medical treatment of a disabled dependant. The maximum deduction under section 80DD is Rs.75,000 for disabled dependants. In case the disabled dependent is a person with severe disability, the maximum deduction allowed is Rs.1.25 lakhs. Deduction under Section 80DD is not dependant on the amount of expenses incurred. Hence, even if the actual expenses on above mentioned disabled dependent relative is less than amount mentioned, full deduction can be claimed under Section 80DD.

Deduction Eligible under Section 80DD

Expenses incurred by the taxpayer to provide medical treatment for a disabled dependant, like nursing, training and rehabilitation of a dependant is can be claimed as a deduction. Also, if the taxpayer made any payment or deposit under a scheme for maintenance of a disabled dependant operated by Life Insurance Corporation or any other insurance company or Unit Trust of India or Jeevan Aadhar Plan, it is admissible as a deduction under section 80DD. However, if an assessee claims deduction under Section 80DD, the disabled dependant should not have claimed deduction under Section 80U.

Individual with Disabled Dependant: An individual taxpayer can claim a deduction under Section 80DD for expenses relating to a disabled dependent, who can be a spouse, son, daughter, parents, brother, or sister.

HUF with Disabled Dependant: If the taxpayer is a HUF, then the deduction can be claimed for supporting a disabled dependent who is a member of the HUF.

Definition of Disability under Section 80DD

"Person with disability" means a person suffering from not less than 40% of any disability mentioned here as certified by a medical authority. The definition for disability under Section 80DD is taken from the "Persons with Disabilities (Equal Opportunities, Protection of Rights and Full Participation) Act, 1995" and "National Trust for welfare of Person with Autism, Cerebral Palsy, Mental Retardation and Multiple Disabilities Act, 1999".

Blindness: "Blindness" refers to a condition where a person suffers from any of the following conditions, namely:- (i) Total absence of sight or (ii) Visual acuity not exceeding 6160 or 201200 (Snellen) in the better eye with correcting lenses or (iii) Limitation of the field of vision subtending an angle of 20 degree or worse.

Cerebral Palsy: "Cerebral palsy" means a group of non-progressive conditions of a person characterized by abnormal motor control posture resulting from brain insult or injuries occurring in the pre-natal, perinatal or infant period of development.

Leprosy Cured Person: "Leprosy cured person" means any person who has been cured of leprosy but is suffering from (i) Loss of sensation in hands or feet as well as loss of sensation and paresis in the eye and eye-lid but with no manifest deformity; (ii) Manifest deformity and paresis; but having sufficient mobility in their hands and feet to enable them to engage in normal economic activity; (iii) Extreme physical deformity as well as advanced age which prevents him from undertaking any gainful occupation, and the expression "leprosy cured" shall be construed accordingly.

Hearing Impairment: "Hearing impairment" means loss of sixty decibels or more in the better year in the conversational range of' frequencies.

Loco Motor Disability: "Loco motor disability" means disability of the bones, joints muscles leading to substantial restriction of the movement of the limbs or any form of cerebral palsy.

Mental Illness: "Mental illness" means any mental disorder other than mental retardation.

Low Vision: "Person with low vision" means a person with impairment of visual functioning even after treatment or standard refractive correction but who uses or is potentially capable of using vision for the planning or execution of a task with appropriate assistive device.

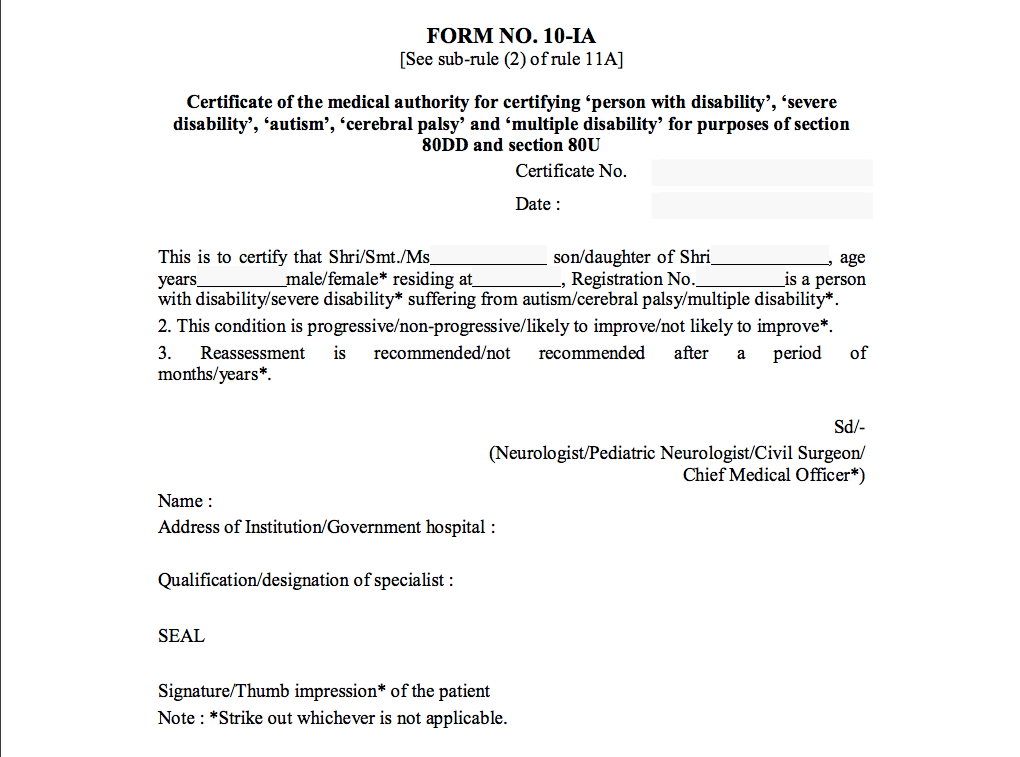

Form 10IA

Form 10IA is a document that must be submitted for claiming section 80DD deduction for disability like autism, cerebral palsy and multiple disabilities. Form 10IA must be signed by a medical authority as follows:

- Neurologist having a degree of Doctor of Medicine (MD) in Neurology (in case of children, a Paediatric Neurologist having an equivalent degree).

- Civil Surgeon or Chief Medical Officer in a Government hospital.

If the condition of disability is temporary and requires reassessment after a specified period, the medical certificate will be valid for the period starting from the assessment year relevant to the previous year during which the certificate was issued and ending with the assessment year relevant to the previous year during which the validity of the certificate expires.

Form-10IA-Format

Form-10IA-Format

Insurance or Deposit for Maintaining Disabled Dependant

Section 80DD deduction can be claimed for insurance or deposits made in a specified scheme to maintain a disabled dependant. The scheme must adhere to the following conditions for an insurance or deposit to be eligible.

Disabled Dependant must Be Nominated.

The assessee nominates either the defendant, who is a person with a disability, or any other person or a trust to receive the payment on his behalf for the benefit of the dependant, who is a person with a disability. If the dependant, a person with a disability, predeceases the individual, an amount equal to the amount paid or deposited shall be deemed to be the income of the assessee of the previous year in which such amount is received by the assessee. It shall accordingly be chargeable to tax as the income of that previous year.