IndiaFilings

Expert

Published on: Jun 24, 2026

Export Bond for GST & Letter of Undertaking

Entities involved in the export of goods having

GST registration are allowed to export goods without payment of IGST by furnishing an export bond or Letter of Undertaking (LUT) in Form GST RFD-11. In this article, we look at this procedure in detail.Letter of Undertaking (LUT) for Exports under GST

According to the Central Goods and Services Tax Rules, 2017, any registered person exporting goods without payment of integrated tax must mandatorily furnish a bond or a Letter of Undertaking (LUT) in FORM GST RFD-11. The following types of persons registered under GST will be allowed to submit a letter of undertaking and undertake export transactions.

- Status holder as specified in the Foreign Trade Policy; or

- Entities that have received the due foreign inward remittances amounting to a minimum of 10% of the export turnover, which should not be less than one crore rupees, in the preceding financial year, and he has not been prosecuted for any offence under the Central Goods and Services Tax Act, 2017 (12 of 2017) or under any of the existing laws in case where the amount of tax evaded exceeds two hundred and fifty lakh rupees.

Letter of Undertaking will be valid for a period of twelve months from the date of submission. If the exporter fails to comply with the conditions of the Letter of Undertaking, the privileges could be revoked and the exporter would be required to furnish a bond. All exporters are required to submit a letter of undertaking or export bond under the new format specified under GST on or before 31st July 2017.

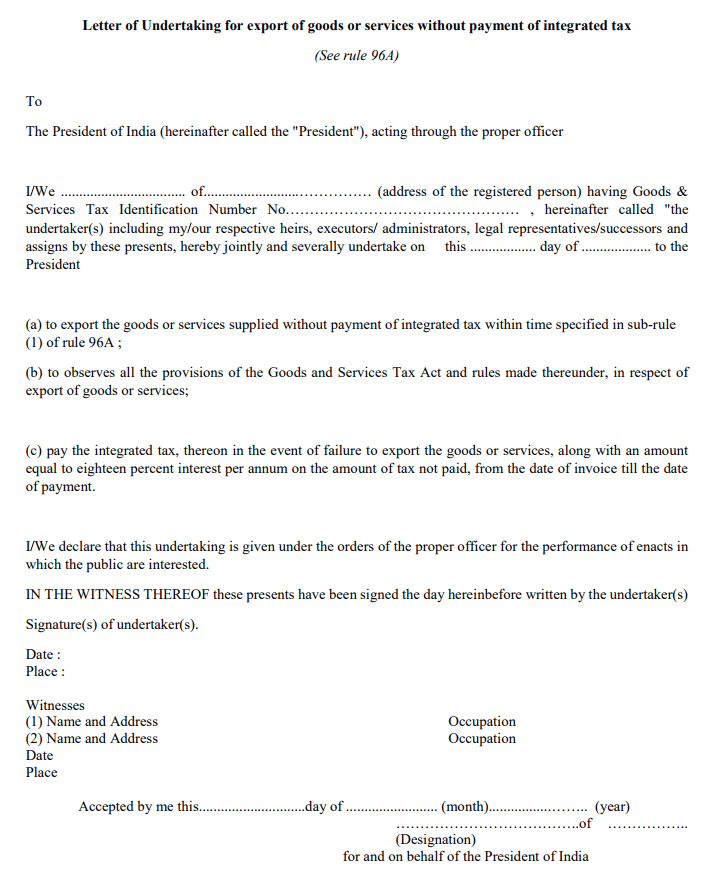

GST Letter of Undertaking Format

The following letter of undertaking format can be adopted by exporters under GST:

GST Letter of Undertaking Format

GST Letter of Undertaking Format

Export Bond for GST

Entities not eligible to submit Letter as per the conditions mentioned above would have to furnish an export bond along with bank guarantee. The bond should cover the amount of tax involved in the export based on estimated tax liability as assessed by the exporter himself. The concerned individual shall furnish the Export bond on a non-judicial stamp paper with the value as indicated in the State. Also, exporters can furnish a running bond, so that export bond need not be executed for each and every export transaction. However, if the outstanding tax liability on exports exceeds the bond amount at any time, then the exporter must furnish a fresh bond to cover the additional liability. The individual shall submit the Export bonds and letter to the jurisdictional Deputy Commissioner or Assistant Commissioner of the concerned jurisdiction. However, after uploading the FORM RFD-11 on the GST Portal, the individual shall proceed to submit the document online.

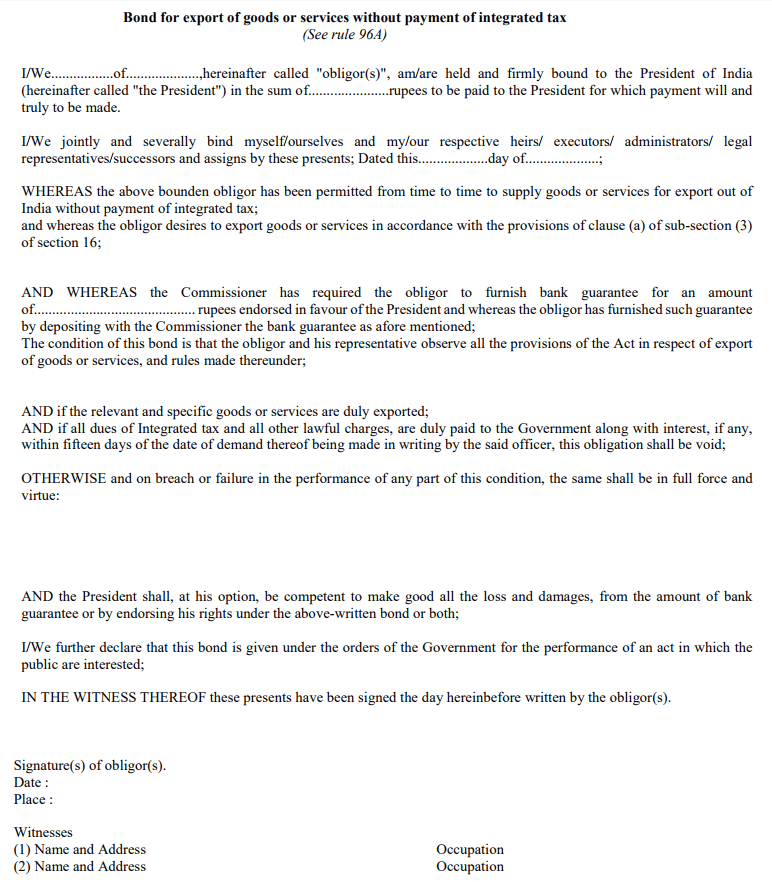

GST Export Bond Format

GST Export Bond Format

GST Export Bond Format

Bank Guarantee for Export Bond

Along with the export bond, the individual shall include a bank guarantee. The value of the bank guarantee should normally not exceed 15% of the bond amount. However, based on the track record of the exporter, the jurisdictional GST Commissioner may wave off the bank guarantee as required along with the export bond.

Import Export Code

The Import Export Code is a primary document necessary for commencing Import-export activities. The IE code is to be obtained for exporting or importing goods or services. IEC has numerous benefits for the growth of the business. Indeed, you cannot ignore the necessity of IE code registration, as it is mandatory. You can apply for an Import Export code through

IndiaFilings and obtain it within 6 to 7 days