IndiaFilings

Expert

Published on: Jul 30, 2026

Calculating Value of Supply under GST

Value of supply is an important concept under GST as it determines the GST payable in a transaction. According to the GST Act, the value of a supply of goods or services is the transaction value, which is the price actually paid or payable for the said supply of goods or services, where the supplier and the recipient of the supply are not related and the price is the sole consideration for the supply. In this article, we look at the process for calculating the value of supply under GST.

Value of Supply

Under GST, the value of supply should always include any taxes, duties, cesses, fees and charges levied under any law except for

IGST, CSGT and SGST, if charged separately by the supplier. In addition, the value of supply must always include:- Any amount that the supplier is liable to pay in relation to such supply but which has been incurred by the recipient of the supply and not included in the price actually paid or payable for the goods or services.

- Incidental expenses, including commission and packing, charged by the supplier to the recipient of a supply and before delivery of goods or supply of services;

- Interest or late fee or penalty for delayed payment of any consideration for any supply; and

- Subsidies directly linked to the price excluding subsidies provided by the Central Government and State Governments.

Discounts NOT to be Included in Value of Supply

The value of supply should not include any discount which is given at any time before or after the supply of goods or services, even if it is recorded in the invoice. As the value of a supply does not include the discount, the input tax credit is not also attributable to the discount on the basis of the invoice mentioning discounts.

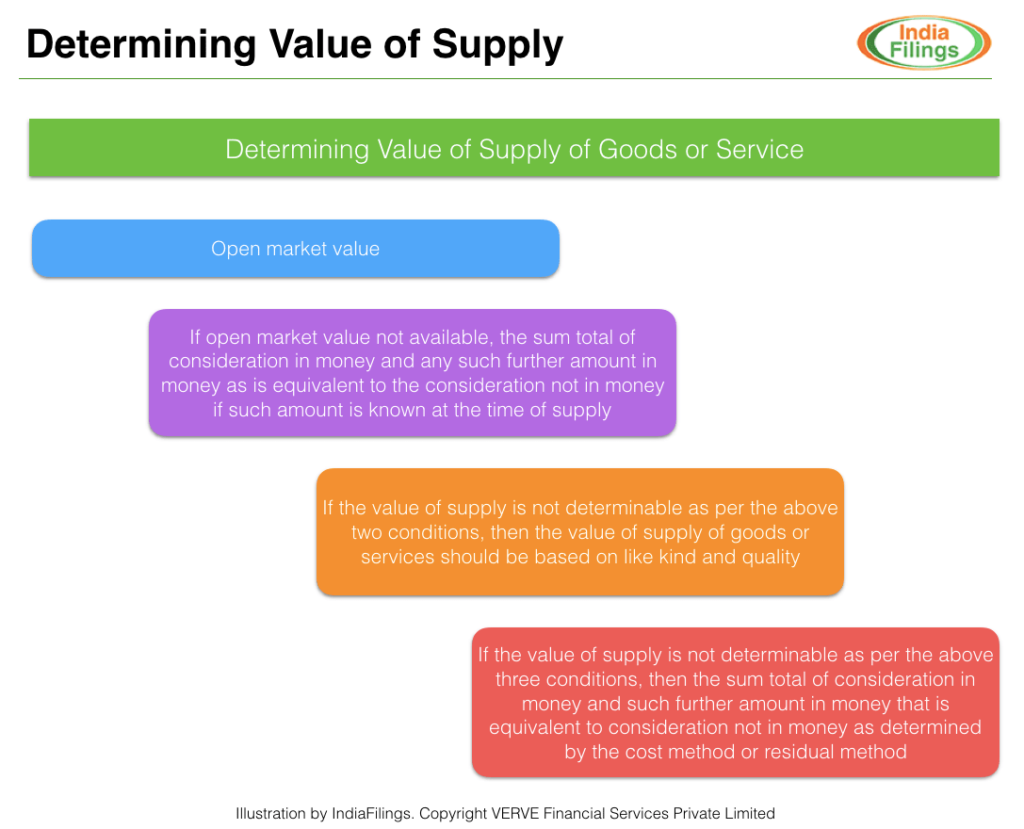

Calculating Value for Supply - Where Consideration NOT Wholly in Money

Value of supply does not include only the amount of money transferred for supply, it also includes consideration not wholly in money, received for the supply of goods or service. While calculating value for supply for goods or services, where the consideration is not wholly in money, the following methodology should be adopted.

First Option: Open Market Value

If the consideration for goods or service is not wholly in money and open market value is available for the goods or services, then the open market value must be adopted as the value of supply. Thus, even if the money transferred would be less, the value of supply and GST payable would be higher based on the open market value.

Second Option: Total Consideration Received during Supply

The second step for calculating value for supply can be adopted if the open market value is not available for a good or service. Under this method, the total consideration of money and the total value of the consideration received during supply, not in money is summed to arrive at the total value of supply. In this methodology, instead of valuing the goods or service supplied, the value of the consideration received is used for calculating the value for supply.

Third Option: Like Kind and Quality If the open market value or the total consideration received method does not work, then the value of a near like kind and quality of goods or service can be adopted as the value of supply.Fourth Option: Total Consideration Received

If the value of goods or service cannot be calculated using any of the above three methods, then the sum total of consideration in money and further amount in money that is equal to consideration not in money should be used as the total value of supply.

Value of Supply under Cost Method

If the value of supply of goods or services cannot be determined by any of the above methods, then the value of supply can be calculated as 110% of the cost of production or manufacturing or cost of acquisition of such goods or cost of provision for such services.

Value of Supply under Residual Method

If the value of supply cannot be calculated even after applying any of the above methods, then the value of supply can be calculated using reasonable means consistent with the principles and general provisions of Section 15 of the GST Act. Also, in case of the supply of service, the service provider can directly use this method instead of using the cost method.

Calculating Value of Supply - For Transaction Between Related Entities

If the value of supply must be calculated for the transaction between related parties, then the following methods can be used in the order of preference as shown in the below illustration:

Determining Value of Supply under GST

Read the Guide on Value of Supply for Related Party Transactions under GST.

Determining Value of Supply under GST

Read the Guide on Value of Supply for Related Party Transactions under GST.

GST Valuation Rules 2017

Valuation of goods and/or service must be according to the GST Act and the Valuation Rules, 2017. The GST Valuation Rules, 2017 is enclosed below:

For more information about GST,

GST registration or GST Filings, contact an IndiaFilings Advisor.